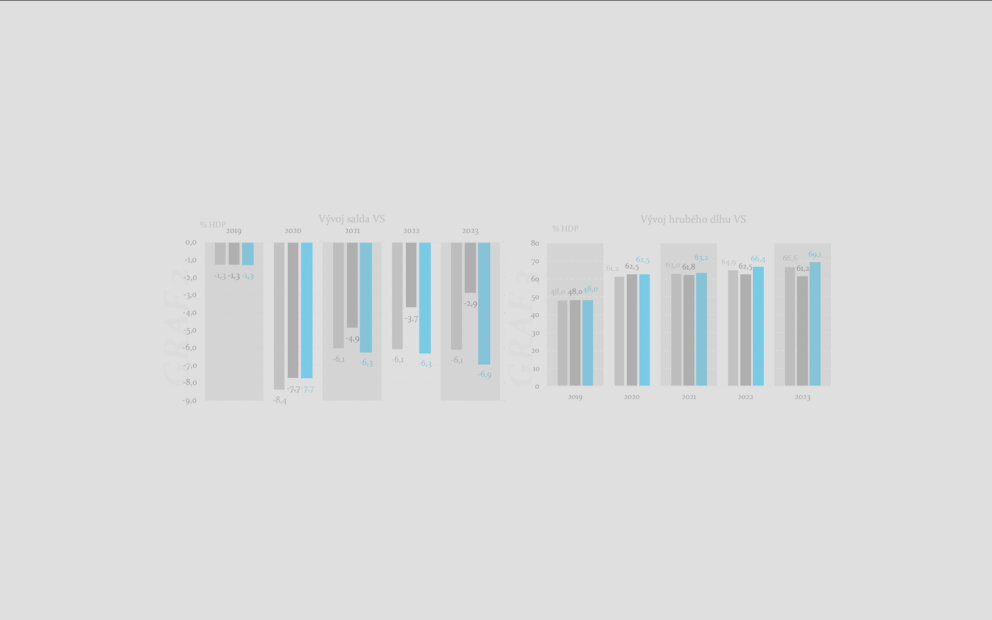

The Ministry of Finance of the Slovak Republic (the Ministry) published an evaluation of compliance with the balanced budget rule for 2018 on 29 November 2019, reporting a significant deviation from the required adjustment path towards the medium-term budgetary objective.