The Council for Budget Responsibility (the Council, CBR) prepared an update to the Evaluation of the General Government Budget for 2026–2028. The addendum assesses changes that occurred after the government approved the draft budget and that affect the expected development of public finances in the coming years, in particular the final design of energy subsidies approved by the government for 2026 and an updated delivery schedule for military equipment, which affects the deficit only at the time of delivery.

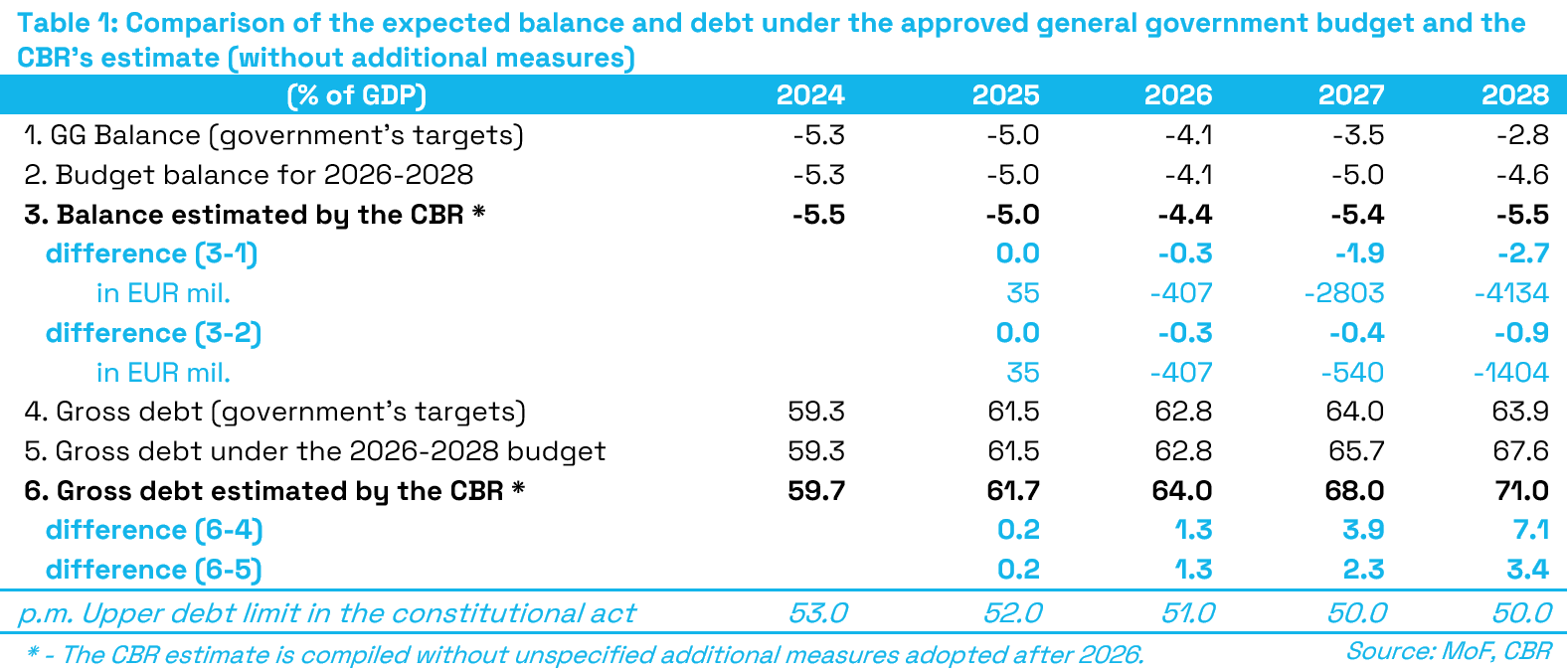

Compared with the government’s proposal, the budget approved by Parliament changed only formally in its structure, while the expected levels of the general government balance in individual years remained unchanged. The approved budget foresees a general government deficit of 4.1% of GDP (EUR 5.9 billion) in 2026; without additional consolidation, a deficit of 5.0% of GDP (EUR 7.6 billion) in 2027; and a deficit of 4.6% of GDP (EUR 7.2 billion) in 2028.

The CBR updated its macroeconomic forecast based on the approved scheme for providing energy subsidies to households and refined statistical information reflecting a deterioration in the macroeconomic environment during the second and third quarters of 2025. The volume and form of the ‘targeted’ subsidies will also be reflected in macroeconomic indicators, particularly through higher inflation. A significant impact stems from the worsening of preliminary data on economic performance in 2025, which also negatively affects expectations for the current year. As a result, the CBR increased its inflation forecast for the coming year to 3.5%. Economic growth below 1% in 2026, which is also the final year of drawing funds from the Recovery and Resilience Plan, mainly reflects the way fiscal consolidation is implemented and unfavourable external developments.

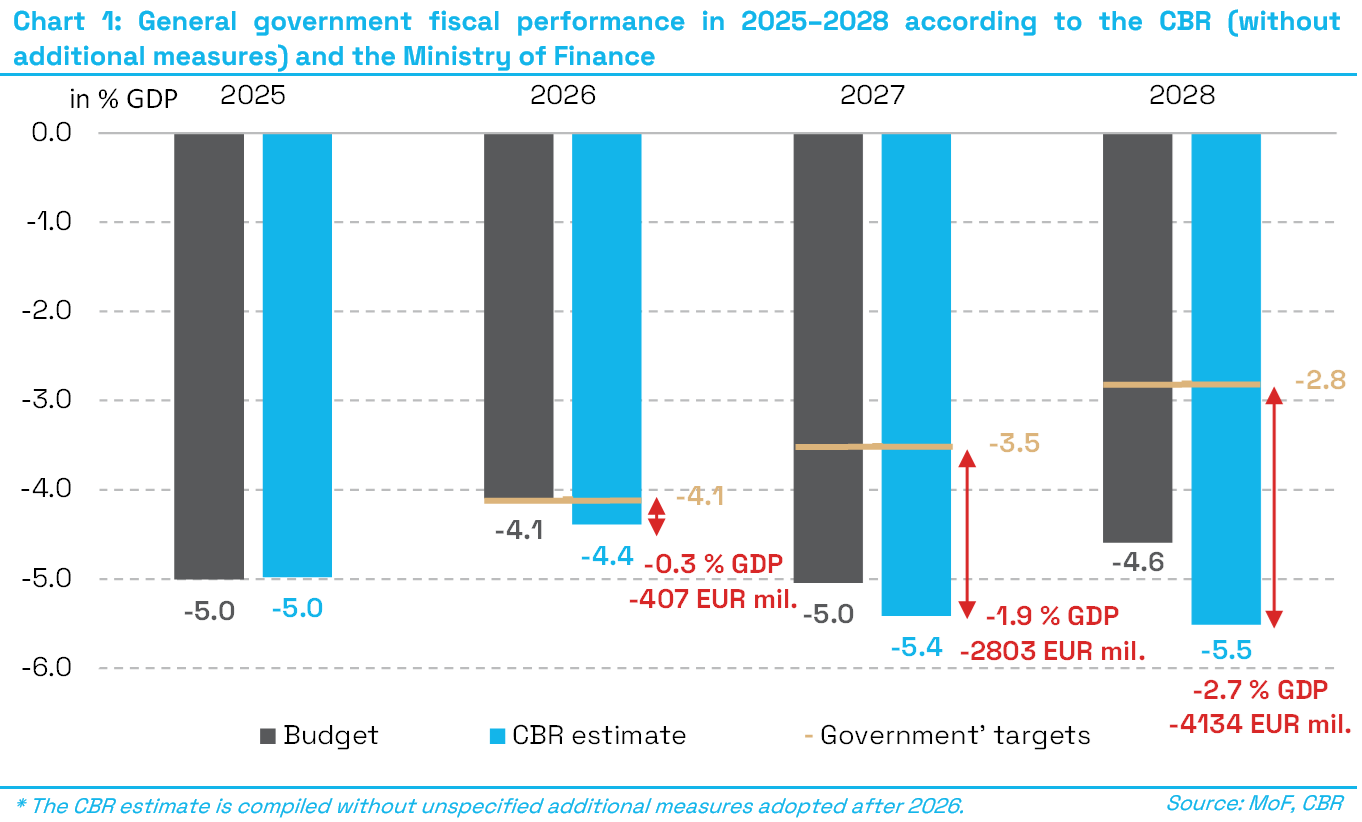

Compared with its earlier assessment of the draft budget, and based on the latest developments and the updated delivery schedule for military equipment, the CBR maintained its estimate of the 2025 general government deficit at 5.0% of GDP. After incorporating these changes, the updated macroeconomic forecast, and new government measures, the CBR revised deficit estimates across the entire forecast horizon. The expected deficit for 2026 was slightly reduced; by contrast, estimated deficits for 2027 and 2028 were increased, mainly due to the assumed postponement of military equipment deliveries and the introduction of a reform of the financing of long-term social and healthcare services. Without additional measures, the general government deficit could reach 4.4% of GDP (EUR 6.2 billion) in 2026, rise to 5.4% of GDP in 2027, and further increase slightly to 5.5% of GDP in 2028.

Following the update of the public finance outlook, the CBR estimates higher deficits than those assumed in the approved budget in every year of the medium-term horizon. In 2026, the negative deviation relative to the budget amounts to 0.3% of GDP (EUR 407 million); in 2027 the difference is 0.4% of GDP; and in 2028 the estimated risk reaches 0.9% of GDP. At the same time, concrete and credible measures to achieve the government’s stated targets are missing in 2027 and 2028. The CBR estimates that, relative to the declared targets, measures amounting to 1.9% of GDP (EUR 2.8 billion) are missing for 2027 and an additional 0.8% of GDP (EUR 1.2 billion) for 2028.

The most significant risk to the budget balance in 2026 is the estimated shortfall in tax and social contribution revenues amounting to EUR 588 million. The bulk of the difference between the CBR’s tax revenue forecast and the approved budget is due to a less favourable assessment of economic developments based on the most recent available information, as the budget is built on older and more optimistic macroeconomic assumptions from September 2025.

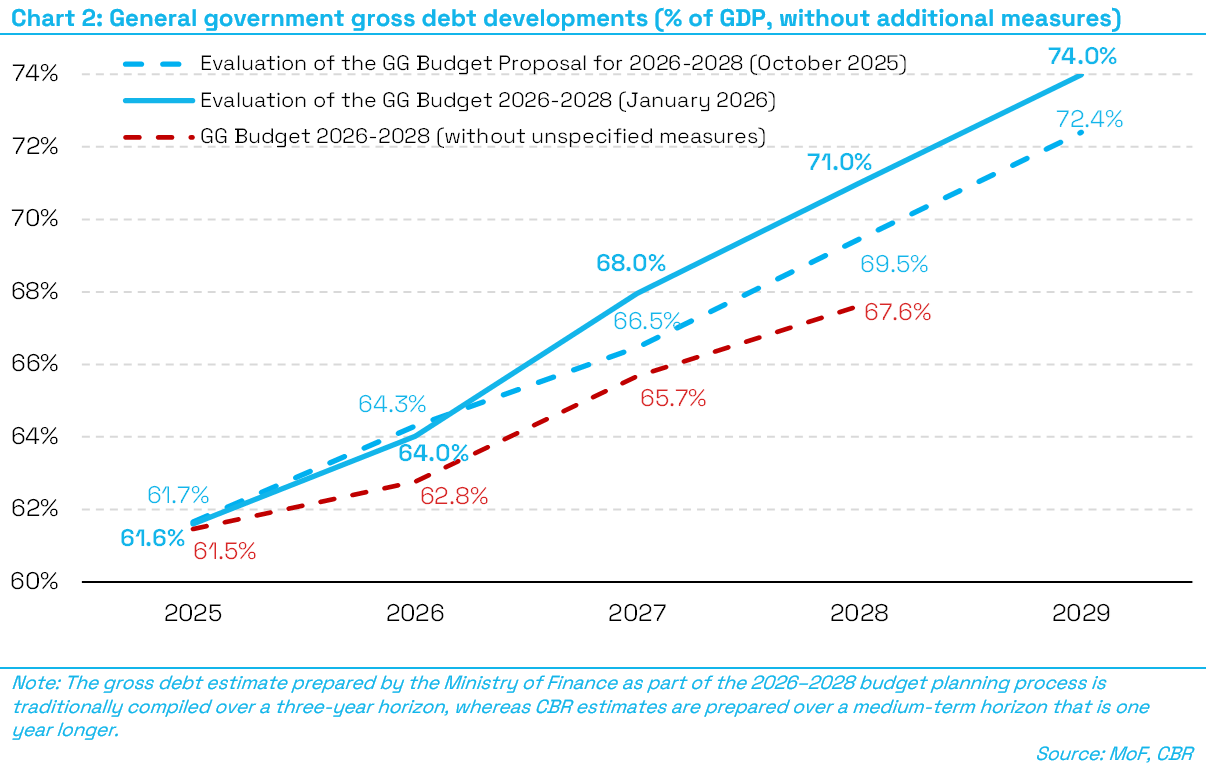

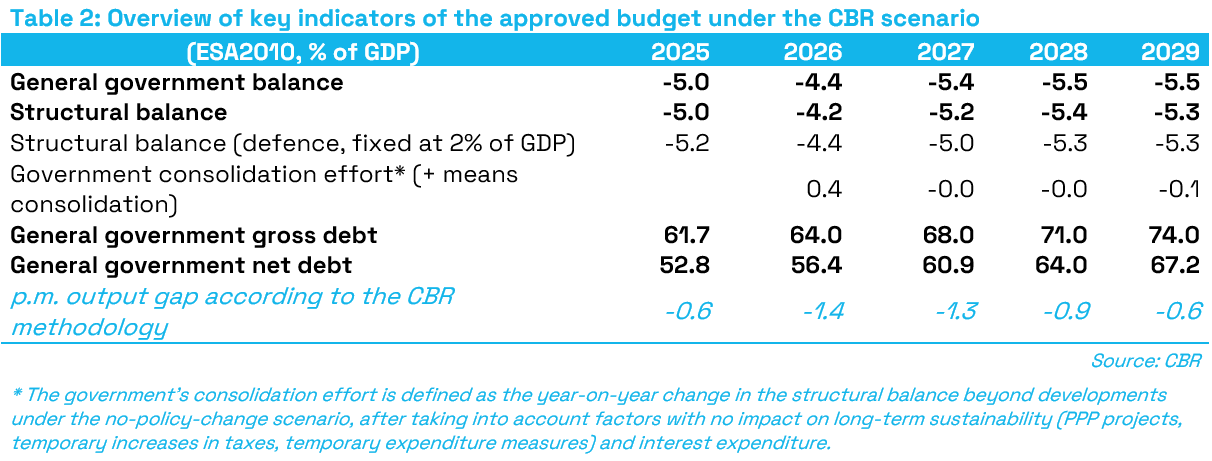

According to the CBR’s estimate, general government gross debt reached 61.6% of GDP in 2025. It is expected to increase further to 64.0% of GDP in 2026 and, in the absence of additional measures beyond the already adopted consolidation, to rise to 74.0% of GDP by the end of the medium-term horizon in 2029. Compared to the evaluation of the budget proposal, in which the CBR estimated gross debt at 72.4% of GDP at the end of 2029, the projected debt-to-GDP ratio has increased mainly as a result of higher estimated deficits over the entire horizon (by 1.2 percentage points of GDP), lower projected GDP growth through the denominator effect, as well as the use of a more appropriate method for estimating the state’s cash reserve between 2027 and 2029. Net debt is estimated by the CBR to have reached 54.7% of GDP at the end of 2025 and is projected to increase to 67.2% of GDP by the end of 2029.

According to the CBR’s estimate, gross debt will remain well above the upper limit of the debt brake throughout the entire forecast horizon, despite the three consolidation packages already adopted. Following the expiry of the escape clause from the application of debt brake sanctions, the sanctions regime was reinstated in full as of 22 November 2025, triggering several obligations for the government under the constitutional act. To date, however, the government has not complied with its obligation to immediately request a vote of confidence from the National Council of the Slovak Republic, nor did it submit a proposal of measures to reduce debt in 2025. Additional sanction measures, including the freezing of salaries of members of the government, are being applied or will be assessed following the publication of the financial statements for 2025.

The expenditure rules (nationally defined nominal expenditure ceilings and net expenditure growth limits under European fiscal rules) will not be sufficiently effective in the coming years. Achieving the maximum permitted expenditure growth through to 2028 while applying the escape clause to defence spending would not be sufficient to meet the primary stated objective of the rules, namely a sustainable reduction of the deficit below 3% of GDP and the stabilisation of debt below 60% of GDP[1]. Although the budget is formally aligned with both expenditure rules in 2026, this does not imply that public finances are being sufficiently consolidated[2].

According to the CBR’s current estimate, the positive contribution of the general government budget to long-term sustainability reaches only a marginal level of 0.1% of GDP (EUR 99 million). Compared to the previous evaluation of the budget, the update of the expected development of public finances prepared by the CBR implies a negative change in the long-term outlook for public finances, driven by permanent expenditure measures adopted by the government. It therefore continues to hold that the measures incorporated in the budget will not ensure a more pronounced decline of the long-term sustainability indicator below the upper bound of the medium-risk zone. At the same time, once the worsened economic developments and the higher deficit in 2025 – i.e. developments preceding the adoption of the budget – are taken into account, an improvement in the long-term sustainability indicator for 2025 may not materialise.

The government’s consolidation effort over the period 2026–2029 is assessed as positive and amounts to a cumulative 0.2% of GDP. This is mainly driven by measures permanently increasing revenues adopted as part of the 2026 consolidation package (higher progressivity of personal income taxation, an increase in health insurance contributions by 1 percentage point for employees, the self-employed and voluntary contributors, and higher taxation of the self-employed). These effects are partly offset by measures permanently increasing expenditure, in particular in the areas of long-term care, old-age pensions and health care.

From the perspective of transparency, the Council considers the most significant shortcoming to be the budget approval process itself, which, given the importance of the document, was disproportionately short. This significantly limited the scope for independent public scrutiny, as well as for Members of Parliament to be adequately informed prior to the budget’s approval. Established practice from recent years was also disrupted, as the CBR was not informed in advance and was not invited in the standard manner to participate in the deliberations of the National Council’s Committee for Finance and Budget. The discussion within the committee was itself shortened. As a result, public and expert debate on the budget was constrained and the quality of parliamentary oversight was reduced.