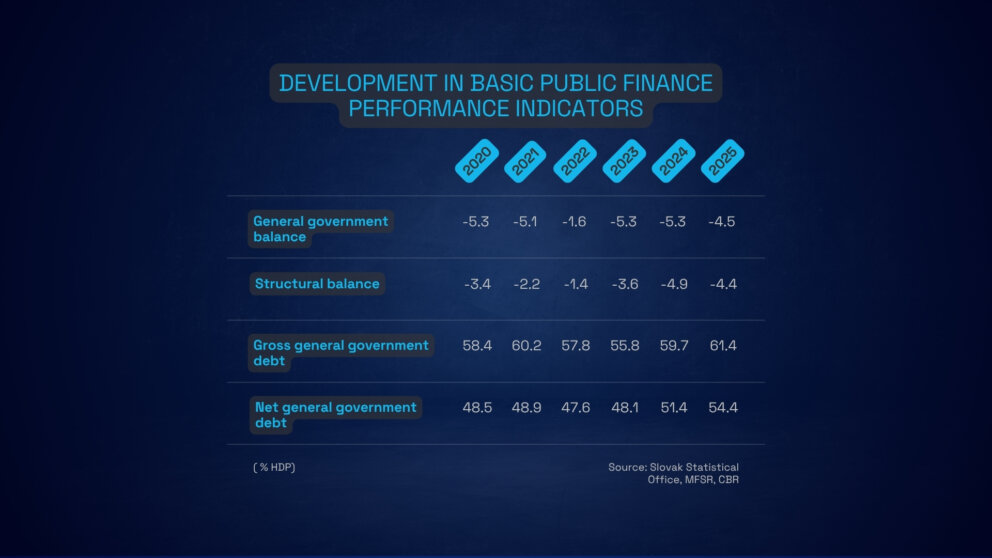

The reformed European fiscal rules were intended to help countries reduce their deficits and debt in a sustainable way. They were adopted in 2024[1], in the period after the Covid-19 pandemic and after the Russian invasion in Ukraine, when the public finances of many countries were under increased pressure. The goal of the rules remains to sustainably reduce deficits below 3% of GDP and debts below 60% of GDP. Since the direct targeting of deficits under the previous rules was not resilient in the face of unexpected crises, the reformed rules introduced a new indicator that EU countries public finances were to follow. This indicator is the maximum net expenditure growth, which in the Slovak case is monitored over a four-year trajectory[2].

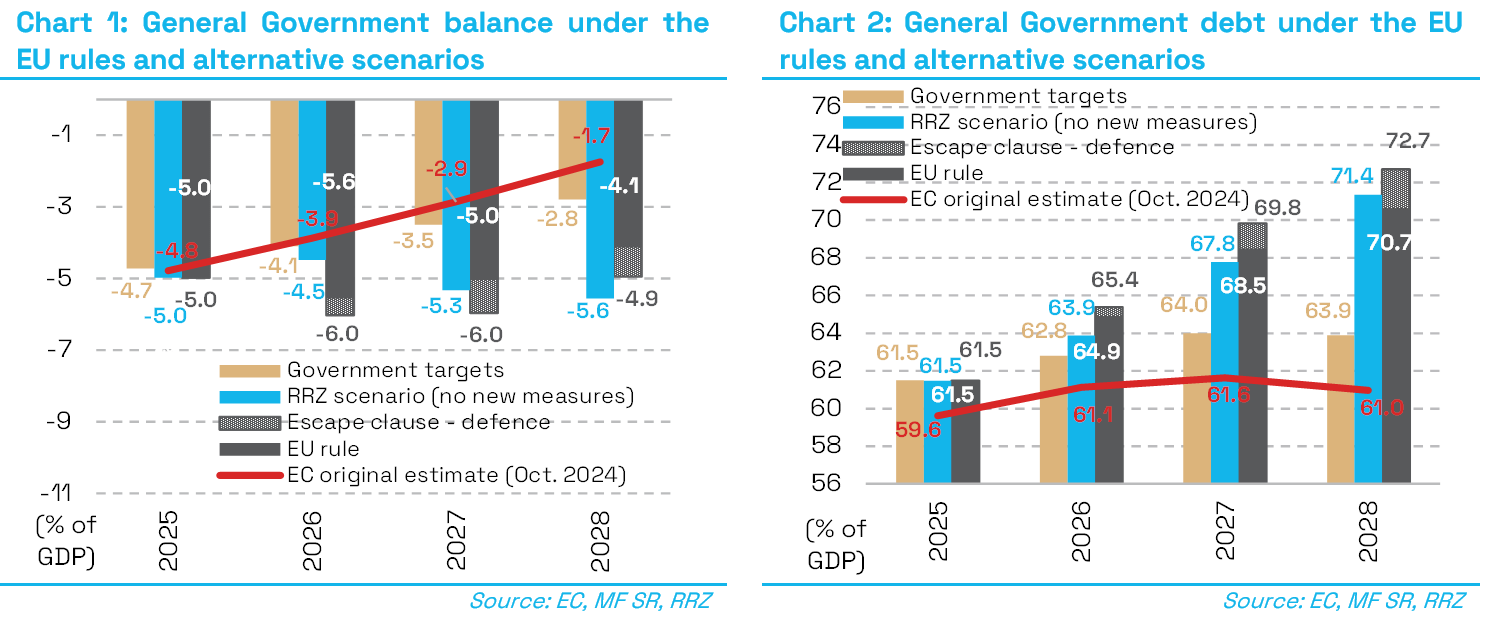

On paper, this is a clear framework; however, at least in the Slovak case, it was set up very loosely from the start, as pointed out by the Council for Budget Responsibility (RRZ) at the time. Progress up to date has confirmed that the net expenditure growth rule is not constructed to achieve sound fiscal consolidation for Slovakia — it will ensure neither debt below 60% nor a deficit below 3% (Charts 1 and 2). Therefore, to fix public finances and halt the unsustainable rise in debt, Slovakia needs its own strategy, since the EU rules – as currently set – are not sufficient for Slovakia.

Slovakia Formally Complies with the New Rules Even with High Deficits and Rapid Debt Growth

The Slovak government accepted the rules by approving the National Medium-Term Fiscal-Structural Plan for 2025–2028 in October 2024, which was endorsed by the Council of the EU in January 2025. The first evaluation of the plan’s implementation by the European Commission will come in spring 2026.

According to current RRZ estimates, Slovakia may comply with the European net expenditure growth rule even if the deficit reaches as high as 6.0% of GDP in 2027. RRZ estimates that without any additional consolidation measures, the deficit could reach approximately 5.3% of GDP in 2027[3].

In other words, the European fiscal rules do not require Slovakia to continue with consolidation in 2027, even though the deficit remains very high.

With such high deficits, debt growth would not stop — on the contrary, by 2028 it would exceed 70% of GDP and continue rising beyond the horizon of the current plan. This directly contradicts the main goal of the European rules, which is to stabilise debt below 60% of GDP[4], and it also contradicts the government’s objective of stabilising debt, what it committed to in its government manifesto.

It is therefore clear that if the government wants to meet its own debt stabilisation objective, it will have to go significantly beyond the loosely set standard required by Brussels. This calls for additional consolidation measures, a better-designed national fiscal framework, and more realistic economic assumptions.

Where Are the Failures? Three Main Reasons Why European Rules Are Not Sufficient

Three key factors lay behind this development in Slovakia with their effects accumulating over time.

1. Unrealistic Expectations of Revenue Growth

The most important flaw was the European Commission’s (EC) assumption that general government revenues would grow at the pace of potential GDP growth in the medium term. This does not hold factually — especially excise taxes and non-tax revenues are not fully elastic to GDP, meaning their share of GDP gradually declines[5]. For example, in 2024 the share of revenues to GDP declined by 0.8 p.p., and according to available estimates, this trend was expected to continue. This overly optimistic assumption therefore assumed a faster decline in the deficit. RRZ pointed out the mismatch between the assumptions and reality already in October 2024, and the same problem was also acknowledged by the Ministry of Finance of the Slovak Republic (MF SR) in the National Medium-Term Fiscal-Structural Plan. Despite this, these risks were not reflected in a stricter setting of the net expenditure growth path, since the MF SR did not request the EC to incorporate more realistic assumptions into the estimate, and the EC itself could not change its assumptions on its own[6]. In practice, this shows that relying on voluntary tightening of the fiscal framework at the national level is not being fulfilled in the Slovak case[7].

2. No Correction of the Limit When Macroeconomic Assumptions Are Not Met

The European Commission set the maximum net expenditure growth for 2024 at 6.2%. This growth was supposed to lead to an improvement in the structural balance of 0.7% of GDP. However, the calculation assumed price growth (measured by the GDP deflator) of 5.7%. Eventually, prices rose only by 3.8%.

Due to the lower-than-expected price growth, actual nominal expenditures grew slower than the rule allowed, but the rule did not reflect this fact in any way. Already in the first year of applying the new rules, this created space for a looser fiscal policy in the future.

The result was a fiscal plan that was inadequate to meet the objectives of the Stability and Growth Pact already at the moment of its approval.

3. Additional Loosening of the Rules Through the Escape Clause for Defence Expenditures

The third factor is the activation of the national escape clause in 2025. The purpose of this exemption is to respond to deteriorating international security. However, defence expenditures often involve a significant lag between the decision and actual implementation[8]. The rule therefore does not only create room for new decisions but also allows countries like Slovakia — which currently has significantly higher defence spending due to decisions made in previous years — to obtain an additional relief from consolidation[9]. As a result of the defence clause, given the expected defence spending, the rule is further loosened by on average 0.6% of GDP in 2025 to 2028.

Combined with the already overly loose baseline rule in Slovakia’s case, this represents another significant relaxation of the fiscal framework. In practice, this means that cumulative compliance with the rule may be adherent “on paper” even when the country’s fiscal position does not actually improve.

European Rules Are Not Sufficient — Responsibility Remains at Home, at the National Level

The government should reconsider the way European fiscal rules are applied at the national level so that they:

- Effectively support a gradual recovery of the Slovak public finances;

- Do not postpone consolidation at the cost of sharp and sudden interventions;

- And at the same time, retain adequate flexibility to react to negative economic and geopolitical shocks.

Without such an approach, there is a threat that the European fiscal rules will remain just a formal exercise and become an incorrect guide for fiscal policy. Any further loosening of even those stricter targets that the government has adopted so far[10] would quickly translate into higher deficits and faster public debt growth. This would limit the country’s ability to respond to future crises and increase risks to public finances, with a direct negative impact on the living standards of the population.

At present, Slovakia lacks an operational budget management rule anchored in the Constitutional Act on Budget Responsibility, aimed at achieving the long-term sustainability of public finances.

[1] This reform replaced previous rules, the so-called Six-Pack, adopted in 2011 and Two-Pack, adopted in 2013.

[2] Member states could choose either a stricter four-year trajectory for their consolidation plan or an extension of the trajectory by a maximum of three extra years, provided that the country concerned committed to implementing reforms and investments improving the growth potential and resilience of its economy.

[3] RRZ, Medium-term Fiscal Outlook (February 2026)

[4] The European Commission’s baseline assumption before the plan (published in October 2024) considered that the deficit would be reduced to 2.5% of GDP by 2027 and to 1.7% of GDP the following year. If these targets were met, the increase in debt would halt and debt would gradually decline and remain below 60% of GDP for the next ten years after the end of the consolidation plan. Based on these targeted deficits, the year-on-year growth in net expenditure for the rule was also derived.

[5] The EC’s assumption also did not consider the temporary nature of some measures adopted during 2023. For example, a temporary increase in employer-paid health contributions, set to expire in 2028, will lead to a reduction in structural revenues. On the other hand, if the government wants to maintain a stable tax-to-GDP ratio by possibly increasing taxes, such an action will automatically be rewarded by an increase in the expenditure limit.

[6] Article 13(b) of Regulation (EU) 2024/1263 of the European Parliament and of the Council specifies that a Member State shall explain the difference if its national medium-term fiscal and structural plan includes a higher net expenditure path than the reference path issued by the Commission, provided that this difference is based on data-based economic arguments. Likewise, opposite deviations proposed by Member States for reasons of prudent budgetary policymaking are generally considered acceptable. There is no legal basis for the Commission to introduce stricter assumptions than in its own framework.

[7] Several countries requested revisions to their assumptions, resulting in a relaxation of the net expenditure growth rate in Estonia, Finland, Greece, Italy and Spain. In the case of France and Romania, the growth rate in the fiscal-structural plan was even tightened compared to the EC recommendation, which was related to different assumptions about the primary structural deficit and different macroeconomic assumptions.

[8] For example, the purchase of fighter jets, which took place in 2018, affects the deficit with a lag of 6 to 8 years.

[9] The escape clause allows for an increase in defence spending by up to 1.5% of GDP in 2025-2028 compared to the 2021 level, when defence spending was only 1.4% of GDP.

[10] The government targeted a deficit of 3% of GDP at the end of the election cycle, which it later reduced to 3.5% of GDP.