Summary

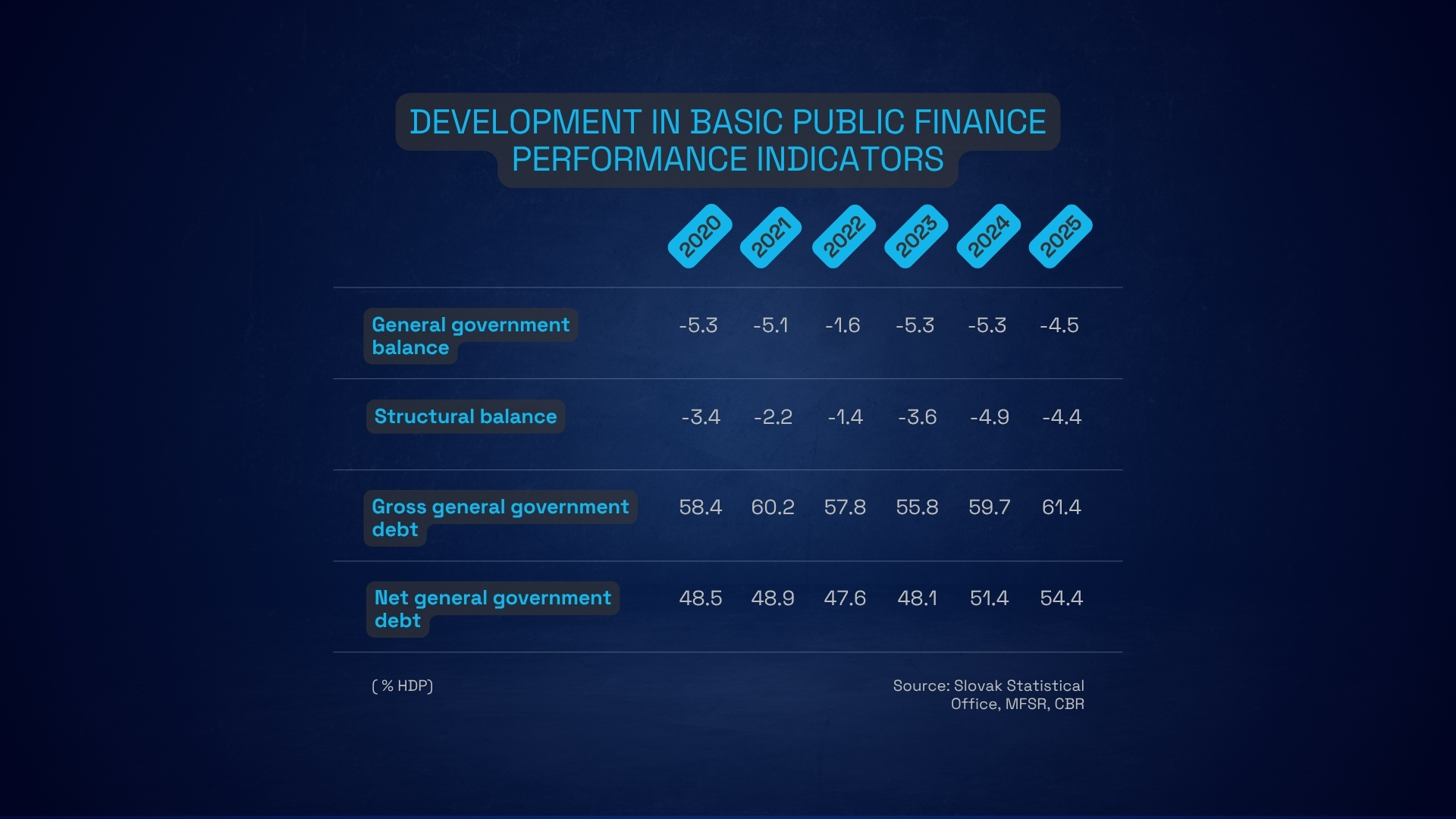

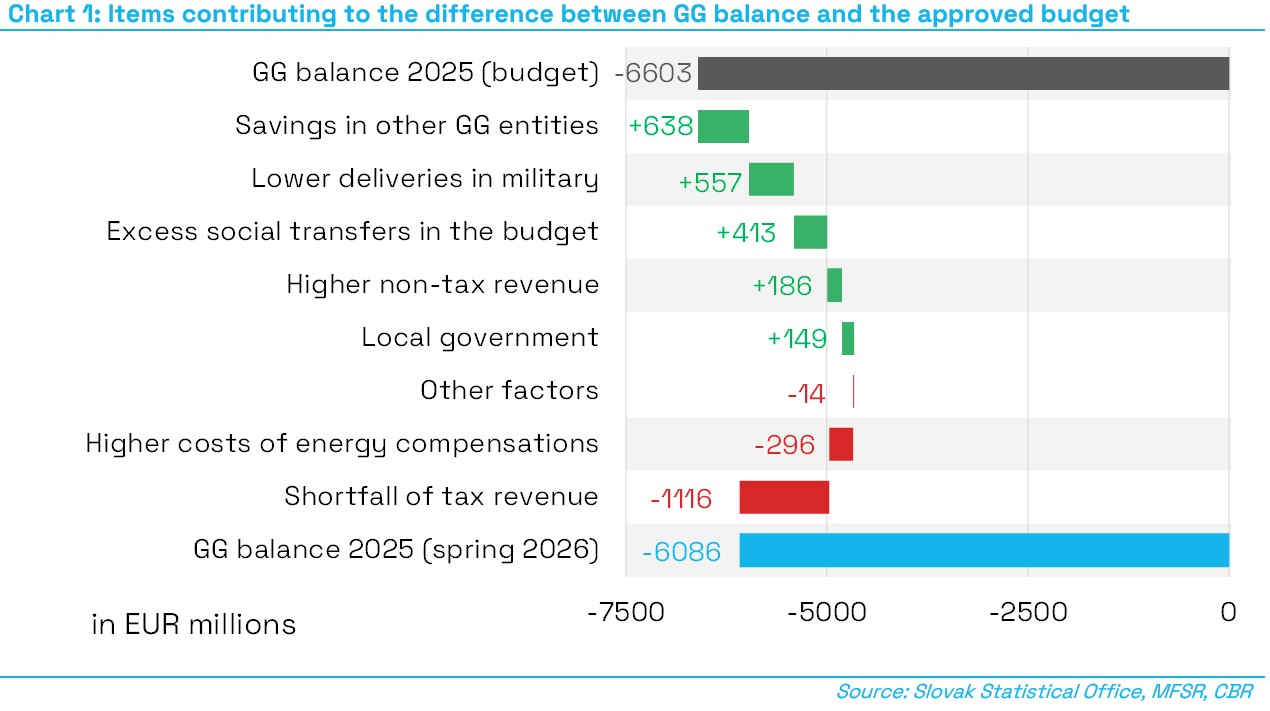

Slovakia’s general government [1] deficit reached 4.5% of GDP in 2025, representing a significant decline of 0.8 percentage points from the high deficit level of the previous year. Compared to the budgeted target of 4.7% of GDP, the final deficit represents a positive deviation of 0.3% of GDP (EUR 368 million), primarily due to delayed deliveries of military equipment, savings in expenditure of other general government entities, and overestimation of social benefits in the budget, which more than offset the strongly negative impact of lower tax and social contribution revenues.

The gross debt, which is less affected by delayed military deliveries, reached 61.4% of GDP. It thus increased by 1.7 percentage points year-on-year, while exceeding the budget assumption by 0.1% of GDP, despite a decline in the cash reserve compared to the budget by almost EUR 1.3 billion (0.9% of GDP). Public debt therefore exceeds the upper limit of the debt brake by as much as 9.4% of GDP, which is a historical maximum. Net debt, i.e. public debt adjusted for the government’s cash reserve, increased by as much as 3 percentage points year-on-year to 54.4% of GDP. Such a pace of increase over the past two non-crisis years exceeds the growth observed during the recent pandemic and energy-security crisis and is comparable only to the period following the outbreak of the global financial crisis.

The largest positive deviation[2] in general government fiscal performance in 2025 compared to the budget was primarily due to lower defence expenditure (0.4% of GDP) and better fiscal performance of general government entities (0.5% of GDP). The budget assumed defence spending at EUR 3.4 billion (2.4% of GDP), while the actual outturn, including accruals, reached EUR 2.7 billion (2.0% of GDP). The recorded savings were mainly related to delays in the delivery of military equipment compared to the budget assumptions[3]. Without lower defence spending, the budget outcome would have been at 4.9% of GDP, worse than the target. These savings can therefore be considered temporary, as delayed deliveries do not represent permanent savings but only a shift to subsequent years.

The better-than-budgeted fiscal result of general government entities was largely due to lower investment spending (especially in the case of ZSSK (railway company) and the Valaliky Industrial Park, as well as transport companies and public universities). These savings also cannot be considered fully permanent, as some of the unspent funds will need to be utilized in the following years.

By contrast, the most significant negative deviation from the budget was caused by lower tax and social contribution revenues (0.8% of GDP). In addition to weaker economic developments, which negatively affected corporate income tax revenues and labor taxation, the shortfall was also driven by lower tax collection efficiency, particularly in value-added tax (VAT). Unlike the temporary positive factors, the revenue shortfall represents a structural deterioration in public finances.

Other factors affecting the balance relative to the budget include the following:

- On the positive side, lower spending on social transfers and benefits contributed EUR 413 million (0.3% of GDP). The savings were mainly due to overestimation of expenditure in the budget, as assumptions regarding the number of newly granted early retirement pensions and recipients of parental benefits were not fulfilled.

- Non-tax revenues improved the deficit by EUR 186 million (0.1% of GDP), mainly due to the first-ever dividend payment by the company Slovenské elektrárne, which had not been included in the budget.

- Another positive contribution came from better fiscal performance of local governments amounting to EUR 149 million (0.1% of GDP), where higher grants and transfers were not fully reflected in increased spending.

- On the negative side, the deficit was affected by energy-related measures with an impact of EUR 296 million (0.2% of GDP). Budgeted resources were insufficient to cover direct costs of energy subsidies, and the deficit impact was further increased by weaker financial performance of MH TH, which was excluded from subsidy schemes, and SPP, where subsidies were partially offset against dividends.

- Unlike previous years, no negative impact on the budget balance from healthcare expenditure was identified in 2025. Higher operating costs of health insurance companies and weaker hospital performance were offset by higher non-tax revenues and lower healthcare spending.

From the point of view of a medium-term burden on public finances, it is better to focus on the structural deficit indicator (i.e., a deficit that will automatically last even into the future, if no additional measures[4] are adopted). In 2025, the structural deficit reached 4.4% of GDP, representing a decrease of 0.5 percentage points compared to 2024. The year-on-year improvement in the structural balance was largely driven by measures adopted by the government, in particular the consolidation package introduced in autumn 2024.

The development of public finances without policy measures, the so-called no-policy-change (NPC) scenario, would imply a deterioration of the structural deficit in 2025 by 0.3% of GDP compared to 2024. The NPC scenario assumes an increase in defence expenditure due to deliveries of military equipment procured in previous years to the level of 2% of GDP (an increase of 0.6 percentage points year-on-year), which would reach the long-term target level for the first time under ESA 2010 methodology. The increase in net interest expenditure (by 0.3 percentage points) would also have a negative impact, reflecting higher interest costs and a decline in temporarily elevated interest revenues. These negative effects would be partially offset by a reduction in social transfers (a year-on-year decline of 0.3 percentage points), mainly due to the decrease in the temporarily increased tax bonus for 2023 and 2024. A lower growth in intermediate consumption (0.2 percentage points) and a slightly faster increase in tax revenues (0.1 percentage points) would also contribute positively.

New measures implemented by the government during the approval of the 2025 budget and throughout the year reduced the structural deficit by 0.7% of GDP. The most significant contribution came from the consolidation package adopted in autumn 2024 (1.2% of GDP), which increased selected tax and non-tax revenues (e.g., changes in VAT rates, higher corporate income tax rates, and the introduction of a financial transaction tax) and reduced selected expenditures (e.g., reduction of the tax bonus and changes to the parental pension scheme). The deficit was also temporarily reduced by lower investment spending (by 0.2 percentage points year-on-year). On the other hand, measures with a negative impact on the structural balance partially offset these improvements, in particular the continuation of broad-based energy subsidies (0.3% of GDP), higher healthcare expenditure and compensation measures (0.2 percentage points), and weaker tax revenues unrelated to policy measures (0.2 percentage points). After adjusting for the temporary reduction in investment spending, the impact of fiscal developments in 2025 on long-term sustainability was positive at 0.5% of GDP[5]. The budget outcome in 2025 therefore implies an improvement in long-term sustainability[6].

In 2025, gross debt reached 61.4% of GDP. After a temporary decline during the high-inflation years of 2022 and 2023 and a renewed increase in 2024, debt continued to rise in 2025, increasing by 1.7 percentage points year-on-year. Gross debt has therefore not yet stabilized and has moved further away from the upper limit of the debt brake.

The main contributors to the year-on-year increase in debt in 2025 were the primary deficit (contributing 2.8 percentage points), interest expenditures related to public debt servicing (1.5 percentage points), and the stock-flow adjustment (1.1 percentage points). Interest costs will represent an increasing burden on public finances in the coming years, as existing debt is being refinanced at significantly higher interest rates compared to the period before 2021.

By contrast, inflation had a mitigating effect on debt dynamics through the denominator effect (−2.4 percentage points). Although its impact increased by almost 0.6 percentage points compared to 2024, it was still insufficient to offset the impact of the primary deficit, unlike in 2022 and 2023 when inflation was in double digits. The decline in the government’s cash reserve also contributed to the increase in debt (0.9 percentage points). Real economic growth had only a limited dampening effect, reducing debt by 0.5 percentage points.

The economy operated slightly below its potential, with a negative output gap of 0.6% of potential GDP. The significant restriction on the revenue side (1.1% of GDP) and current expenditure (1.1% of GDP) was partially offset by higher capital expenditure (0.8% of GDP) and increased absorption of EU funds (0.4% of GDP), particularly the Recovery and Resilience Plan. The fiscal impulse in 2025 had a restrictive impact on the economy amounting 1.0 % of GDP.

From the perspective of long-term sustainability, economic growth over a longer horizon plays a key role. This can be supported by the accumulation of new capital through effective public investment. As the flow of EU funds follows a multiannual absorption plan and the schedule of the relevant programming period, it is important from a fiscal management perspective to monitor the development of domestic public investment. At the same time, it is appropriate to adjust these investments for expenditure on military equipment, as their recorded level in the budget balance under ESA 2010 is largely influenced by delivery schedules.

In 2025, public investment excluding defence and EU funds declined year-on-year to 2.2% of GDP. This represents a decrease of 0.3 percentage points compared to the 10-year average, 0.1 percentage points compared to the previous year, and 0.1 percentage points below the budget assumptions. Lower investment contributed to a reduction in the deficit compared to the budget by EUR 144 million (and by EUR 399 million compared to the 10-year average). Compared to the V3 average[7], public investment excluding defence and EU funds is lower by as much as 1.2 percentage points of GDP, corresponding to EUR 1.6 billion.