The government approved the 2026 Annual Progress Report of the Slovak Republic (hereinafter referred to as the “annual report” or “report”), in which it evaluates the ongoing implementation of the National Medium-Term Fiscal-Structural Plan of the Slovak Republic for 2025-2028. In the report, the government also updated the general government deficit targets for the upcoming period.

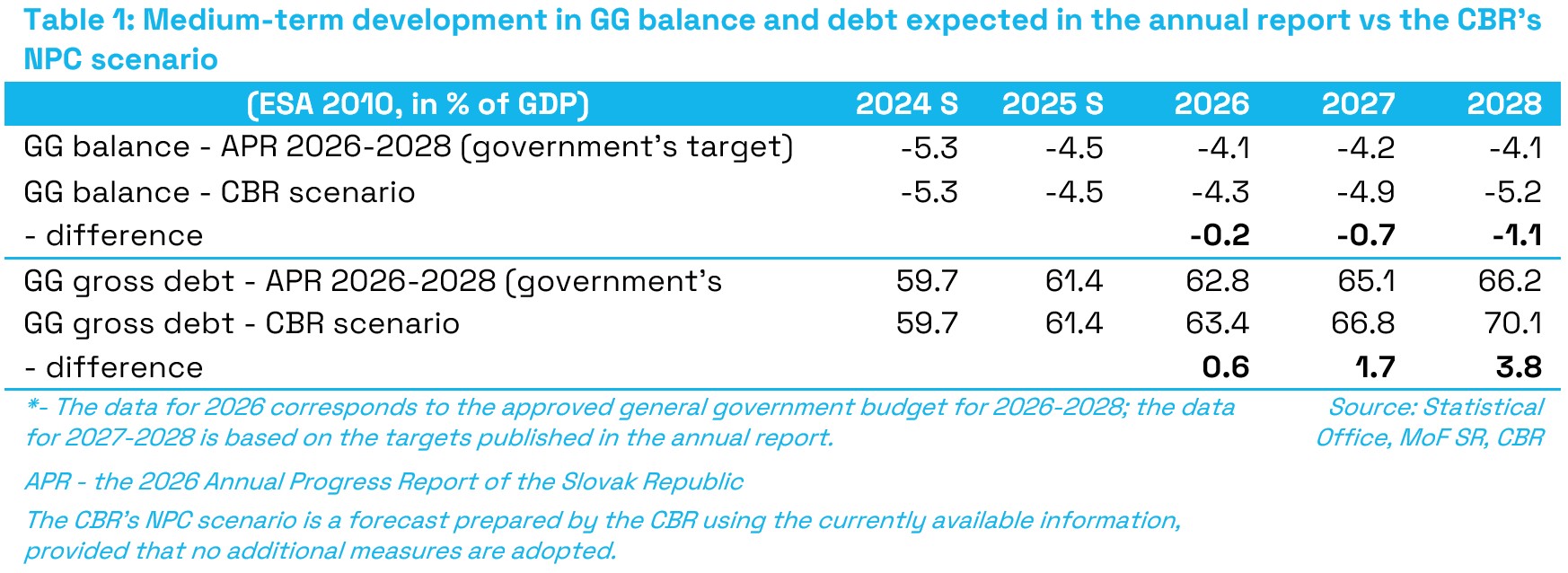

The medium-term budgetary objectives proposed by the government expect the general government deficit to gradually decline to 4.2% of GDP in 2027 and 4.1% of GDP in 2028. Compared to the approved budget for 2026 to 2028, this represents a significant relaxation of budgetary targets, as the budget originally expected the deficit to decline to 2.8% of GDP in 2028.

Unlike in previous years, government report for the first time does not publish the expected development of general government revenue and expenditure without measures (the so-called fiscal outlook), which significantly reduces the transparency of the report. It is therefore not clear what extent of consolidation measures the government expects in the coming years. At the same time, the annual report continues to lack specific measures that would ensure the achievement of the updated budgetary objectives.[1]

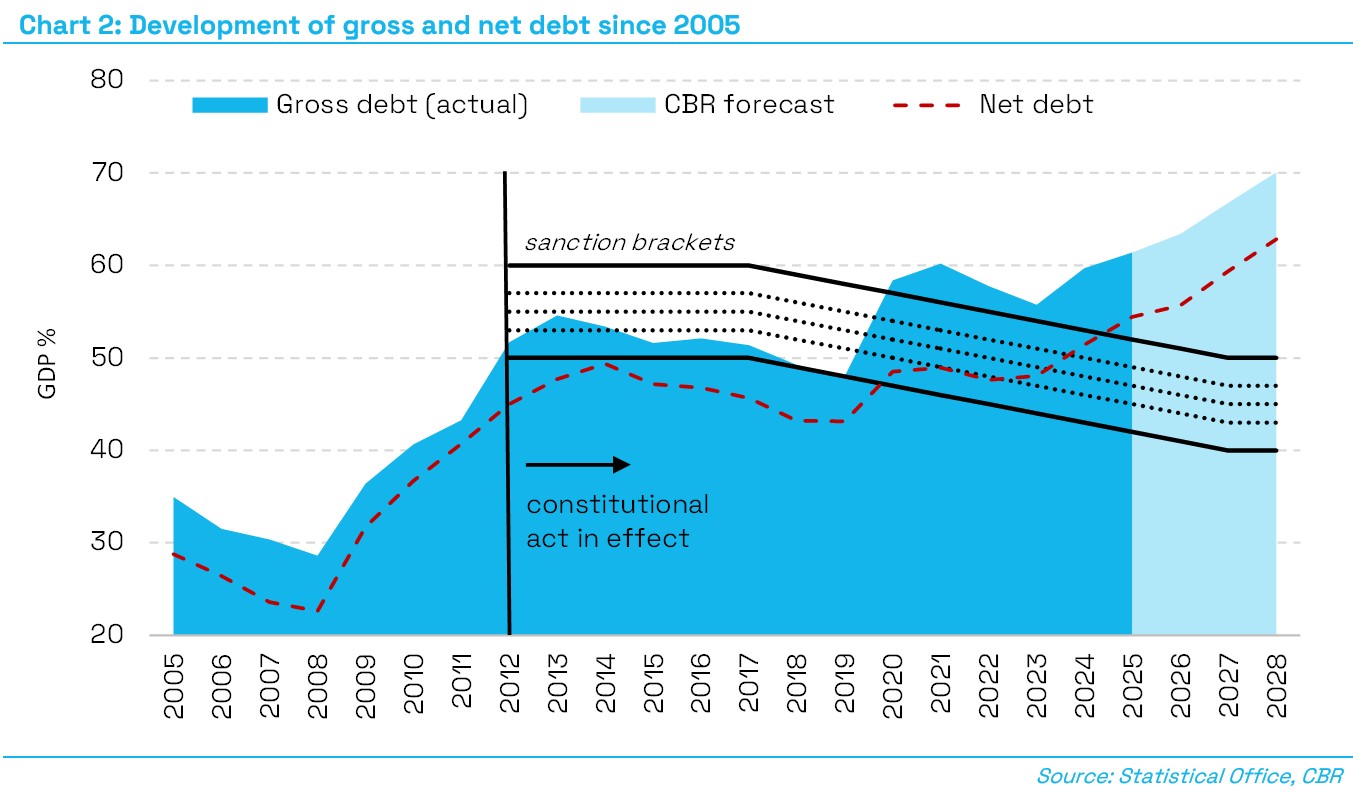

Assuming that the deficit targets are met, the government expects gross debt to continue increasing from 61.4% of GDP in 2025 to 66.2% of GDP at the end of 2028. The increase is mainly driven by persistently high deficit levels in the near term. Notwithstanding the targeted moderation of debt growth after 2024, debt has remained above the upper threshold of the sanction brackets under the constitutional Fiscal Responsibility Act since 2020, is expected to remain above this threshold throughout the entire forecast period and is reaching historically high deviations.

The purpose of the opinion prepared by the Council for Budget Responsibility (CBR, Council) is to offer an independent view on the budget outline and assess whether the current fiscal policy set-up is sufficient to achieve the targets set in the annual report. In accordance with its mandate, the CBR also highlights whether the government’s current fiscal outlook creates the conditions for ensuring the long-term sustainability of public finances and compliance with national fiscal rules.

Assessment of the medium-term outlook

The medium-term budgetary objectives proposed by the government relax the deficit targets compared to the approved budget; the government is thus abandoning the ambition to reduce the general government deficit towards 3.0% of GDP, while it was originally envisaged that this target would be achieved by 2027. Compared to the budgetary objectives presented in the approved budget, the government’s current deficit targets have been significantly increased by 0.7% of GDP in 2027 and by 1.3% of GDP in 2028. The government justifies the relaxation of targets by adverse geopolitical factors; however, the annual report does not contain a more detailed calculation.[2]

According to the Council, a relaxation of budgetary targets may be justified to some extent if the risks of economic deterioration materialize. In such a case, the degree of relaxation should be proportionate and verified by an independent estimate of the Macroeconomic Forecasting Committee, which has not yet happened. At the same time, the Committee’s macroeconomic forecast from February, which was used in the report, does not directly imply the need to relax the target. For this reason, the Council considers this step premature and unjustified.[3]

In its annual report, the government does not specify how the relaxation of budgetary objectives compared to the approved budget relates to the negative impacts of the conflict in the Middle East estimated under the risk scenarios. New expenditure that does not directly result from geopolitical risks but is related to new government policies should not lead to a relaxation of deficit targets; instead, it should be fully offset by austerity measures with no impact on the budgetary objectives.

The year 2026 is the baseline year for setting the budgetary objectives for 2027 and 2028 presented in the annual report. According to the Council, the general government deficit could reach 4.3% of GDP (EUR 6.1bn) in 2026, thus exceeding the target under the approved budget by 0.2% of GDP (EUR 250mn). Compared to the government’s current estimate, this represents almost the same starting position, with a slightly positive risk mainly related to a better estimated performance of other general government entities as well as lower absorption of state budget expenditure. As regards medium-term developments under the no-policy-change (NPC) scenario, the CBR expects the deficit to amount to 4.9% of GDP in 2027, followed by an increase to 5.2% of GDP in 2028.[4]

Compared to the declared relaxed deficit target of 4.2% of GDP for 2027, the government lacks specified measures worth 0.7% of GDP (EUR 1.0bn), according to the CBR. Although the targeted deficit remains almost unchanged year on year, this amount of consolidation will be necessary to offset negative impacts such as rising interest costs, defence expenditure caused by delayed deliveries, as well as new expenditure measures (costs related to the long-term care reform).[5]

In 2028, which is beyond the horizon of the current electoral term, achieving the budgetary objective set by the government at 4.1% of GDP would require the adoption of additional measures amounting to 0.4% of GDP (EUR 0.7bn). In view of the expiry of temporary measures, further consolidation measures would be needed in 2028 even to keep the deficit at an unchanged level.[6]

The CBR estimates that, without measures, the structural deficit, net of the impact of economic fluctuations and other one-off and temporary measures, will gradually increase over the entire medium-term horizon from an estimated 4.1% of GDP in 2026 to 5% of GDP in 2028. Rising interest costs, as well as the expiry of previously adopted government measures with a temporary positive impact on the GG balance, will be reflected in an increase in the structural deficit over the coming period.

Considering the estimated development of balance, the CBR expects gross debt to reach 70.1% of GDP at the end of the medium-term horizon in 2028. Net debt will reach 62.9% of GDP at the end of 2028. The government’s performance (primary deficits) will be the most significant factor behind the sharp rise in debt over the entire horizon. Cumulatively, without additional consolidation, primary deficits will contribute to an increase in gross debt by approximately 8.9 p.p. of GDP. In order to stabilize gross debt at around 65% of GDP, it would be necessary to continue reducing the general government deficit until 2028, to approximately 2.4% of GDP.

As the sanction brackets of the debt brake will be declining annually to finally arrive at 50% of GDP in 2027 (for the highest sanction bracket), the gap between the expected gross debt level and the highest sanction bracket of the debt brake will keep widening. At the end of the medium-term horizon in 2028, gross debt would thus exceed the highest sanction bracket of the debt brake by as much as 20.1 p.p. of GDP.

The long-term sustainability of public finances is in the high-risk zone. The value of the indicator reached 5.5% of GDP at the end of 2025[7]. If the government met its budgetary objective for 2027 through measures permanently improving public finances in the required amount of 0.7% of GDP, long-term sustainability could move to the boundary between the medium-risk and high-risk zones.[8]

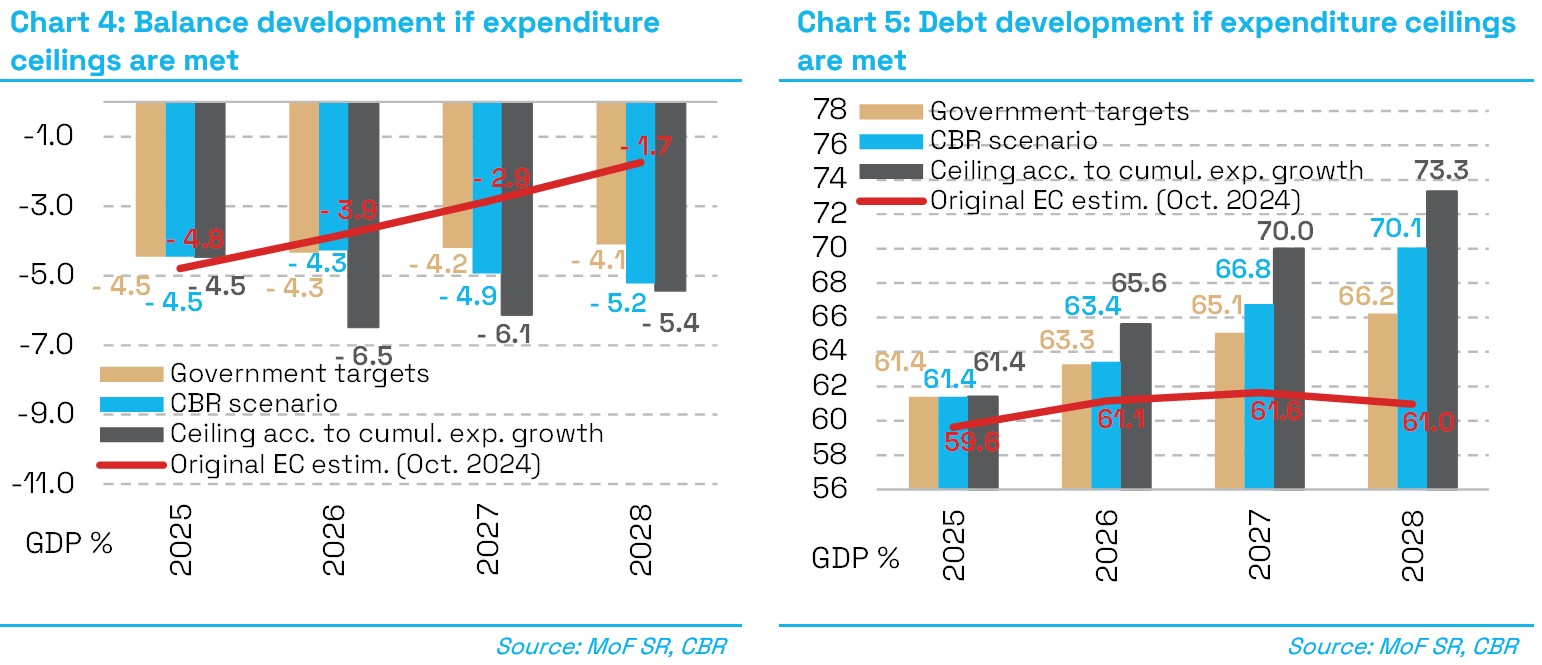

Compliance with the European fiscal rules in the form of the maximum net expenditure growth rate is not sufficient to reduce the deficit below 3% of GDP or to stabilise debt below 60% of GDP. The CBR estimates that even without continuing the consolidation of public finances, the rule would be formally met by 2028[9] (by 0.1% of GDP after considering the defence exemption[10]). The CBR has long warned about the flawed setup of the European rule for Slovakia[11], which does not require continued consolidation and even allows the sharp increase in debt to continue.[12]

As far as the European rules are concerned, the CBR estimates that, if government expenditure were to grow exactly in line with the mandatory path, the deficit could reach 6.5% of GDP in 2026, declining only to 5.4% of GDP by 2028. In such a case, debt would rise sharply and would already reach 73.3% of GDP in 2028, which is as much as 3.3 p.p. higher than estimated in the current CBR scenario.[13]

The non-publication of the fiscal outlook for the next three years significantly reduces the transparency of the budgetary process compared to the past. From the publication of the approved three-year budget for the previous period (2026 to 2028) at the end of 2025 until probably October 2026, when the government submits the draft budget to the National Council of the Slovak Republic pursuant to the Act, no comprehensive updated data from the Ministry of Finance on the medium-term outlook for public finances will be publicly available.[14]