The government approved the 2025 Annual Progress Report of the Slovak Republic (hereinafter referred to as the “annual report” or “report”), evaluating the initial implementation of the National Medium-Term Fiscal-Structural Plan of the Slovak Republic for 2025-28. In the report, the government specified general government deficit targets for the upcoming period and also presented an updated fiscal outlook for the performance of the general government (i.e. budget execution without additional measures).

The document provides information on the direction of fiscal policy and the amount of measures, as envisaged by the government, which are necessary for meeting the declared budgetary objectives. In the document, the government also requests that the European Commission apply a national escape clause from the EU fiscal rules to increased defence spending[1].

The medium-term budgetary objectives proposed by the government expect the general government deficit to gradually decline to 2.8 % of GDP in 2028, but the annual report lacks specific measures to fully achieve these objectives. At the same time, the budgetary objectives have been relaxed compared to the approved budget by 0.4 % of GDP in 2026 and by 0.5 % of GDP in 2027.

In the government’s fiscal outlook, the deficit will increase from the level expected for 2025 at 4.9 % of GDP to 5.3 % – 5.8 % of GDP in the period between 2026 and 2028, mainly due to the projected impact of fiscal risks.

The fiscal outlook (without additional measures) expects the gross debt to increase from 59.3 % of GDP in 2024 to 68.9 % of GDP at the end of 2028. The increase is mainly driven by the high levels of deficits expected in the near term. Assuming that the budgetary objectives are met, gross debt would be growing at a slower pace after 2025, reaching the level of 62.3 % of GDP at the end of 2028. Notwithstanding the targeted debt growth reduction after 2024, the debt has remained above the upper threshold of the sanction brackets under the constitutional Fiscal Responsibility Act since 2020, and is expected to remain above this threshold throughout the entire forecast period.

In line with the obligations under Section 30(4) of Act No. 523/2004 on general government budgetary rules (hereinafter as the “Act”), the purpose of the opinion prepared by the Council for Budget Responsibility (CBR, Council) is to assess compliance of the budget outturn with the public expenditure ceiling and the net expenditure development path. The CBR hopes to offer an independent view on the budget outline presented in the annual report and assess whether the fiscal policy setup is sufficient in terms of achieving the targets set and, at the same time, to identify potential risks which need to be eliminated through the adoption of additional measures. In accordance with its mandate, the CBR also assesses whether the current fiscal outlook of the government creates the conditions for ensuring the long-term sustainability of public finances and compliance with national fiscal rules.

In this context, the Council highlights the following main conclusions from its assessment:

- When evaluating compliance with the nominal public expenditure ceiling (the national rule) and the net expenditure growth rate (the European rule) for 2024, the Council has arrived at different conclusions, indicating that these rules are inconsistent with each other. Because the nominal ceiling is used as an operative budget-management tool[2], it is important that its amount flexibly reflects any changes in the assumptions on which it was calculated.

- The nominal value of the public expenditure ceiling for 2024 was set by law at EUR 57.7bn. According to the CBR, the public expenditure ceiling has been exceeded by EUR 189mn based on the most recent data[3]. In its assessment, the Ministry of Finance of the Slovak Republic noted that the ceiling for 2024 was achieved with a margin of EUR 112mn. The difference compared to the CBR’s assessment is primarily due to the fact that the Ministry of Finance used, as an estimate of expenditure funded from the EU budget, the data provided by the Statistical Office of the Slovak Republic, which – as opposed to the CBR’s estimate – did not take into account some necessary adjustments, in particular the correction of incorrectly reported energy subsidies because, in 2024, these were financed from national sources rather than from EU funds.

- The maximum allowed net expenditure growth for 2024, set on the basis of the national medium-term fiscal-structural plan endorsed by the Council of the European Union, was not allowed to exceed 6.2 %. The CBR notes that the net expenditure growth stood at 3.8 %, thus meeting the year-on-year net expenditure growth rule by 2.4 p.p. (EUR 1.3bn). The lower net expenditure growth rate was mainly due to a substantial year-on-year reduction in the expenditure on energy subsidies. However, this does not involve an active reduction based on a government policy, but only a result of lower market prices compared to the extreme levels seen in the previous year. Without this factor, the rule would not have been met in 2024.

- The final assessment of this rule depends on the quality of the input data, with different results that can be arrived at based on the choice of the source of the data used. In 2024, net expenditure growth rate stood at 3.0 % according to the assessment prepared by the Ministry of Finance and, according to the European Commission, at 5.4 %. In general, the input data for the calculation of net expenditure growth should be unambiguous and independently assessed; however, this is currently not the case for some items. The most significant category covers the funding from the EU budget including co-financing. Considering that compliance with this rule is not subject to any sanctions[4] yet, there is still room for improving the preparation of data and standardising the procedure for their quantification in calculating the net expenditure growth rate in the near term.

- With the medium-term budgetary objectives proposed by the government, the deficit targets are being relaxed compared to the approved budget, whereas a reduction of the general government deficit to 3.0 % of GDP is foreseen by 2028 rather than 2027, as originally envisaged. Compared to the budgetary objectives presented in the approved budget, the government’s most recent deficit targets have currently been increased by 0.4 % of GDP for 2026 and by 0.5 % of GDP for 2027. The government justifies the relaxation of targets by adverse geopolitical factors; however, the annual report does not contain more detailed calculation.

- According to the Council, partial relaxation of the budgetary objectives may be justified in view of the economic downturn, but the degree to which these targets are relaxed should be proportionate and verified by an independent estimate of the Macroeconomic Forecasting Committee. The CBR estimates that, in the event of major international trade restrictions, the deficit could worsen by as much as 0.4 % of GDP by 2027. If a partial agreement is reached, which is the more likely case, the negative effects would be significantly milder.

- In its annual report, the government does not specify how the relaxation of the budgetary objectives compared to the approved budget relates to a shortfall in revenue under the no-police-change fiscal outlook. New expenditure, albeit not directly associated with geopolitical risks but related to new government policies, should not result in the relaxation of the deficit targets, but rather be fully offset by austerity measures having no impact on the budgetary objectives.

- The year 2025 is the baseline year for setting the budgetary objectives between 2026 and 2028, as presented in the annual report. According to the Council, the general government deficit could reach 5.0 % of GDP (EUR 6.9bn) in 2025, thus exceeding the target under the approved budget by 0.3 % of GDP (EUR 405mn). Compared to the government’s most recent estimate, this represents a slightly worse starting position (by 0.1 % of GDP), with the negative risk being primarily due to the higher absorption of capital expenditure in the state budget, as well as lower tax and contribution revenues.

- For the medium-term development under the CBR’s scenario, i.e. preserving the existing policies, the CBR expects the deficit to amount to 5.3 % of GDP in 2026 and 5.2 % of GDP in 2027, with a subsequent rise to 5.7 % of GDP[5] in 2028 followed by a slight decline to 5.6 % of GDP in 2029. Compared to the government’s fiscal outlook, the deficit levels estimated for 2026 are the same, whereas the 2027 deficit foreseen by the CBR is lower by 0.6 % of GDP in comparison with the fiscal outlook; however, in 2028, it is higher by 0.2 % of GDP.

- Taking into account the declared targets to reduce the deficit to 2.8 % of GDP by 2028, the government needs to specify measures worth 1.2 % of GDP (EUR 1.8bn) in 2026, 1.7 % of GDP (EUR 2.6bn, i.e. an additional EUR 0.8bn) in 2027, and 2.9 % of GDP (EUR 4.6bn, i.e. an additional EUR 2bn) in 2028, according to the CBR. In view of the expiry of the temporary measures after 2027, maintaining the deficit at an unchanged level will also require the adoption of further consolidation measures in 2028.

- With no measures adopted, the CBR estimates that the structural deficit, net of the impact of economic fluctuations and other one-off and temporary measures, would increase over the entire medium-term period from 4.8 % of GDP in 2025 to as much as 5.6 % of GDP in 2028. In addition to higher defence spending, this increase will also be driven by the costs of government measures adopted in 2025, expiry of temporary revenue-side measures in 2028, as well as an increase in interest payments.

- Considering the estimated development of balance, the CBR expects the gross debt to reach a level of 71.4 % of GDP at the end of the medium-term horizon in 2029. The net debt[6] will be at 65.3 % of GDP at the end of 2029. Over the entire horizon, the government’s primary deficits will be the most significant factor behind a sharply rising debt. Without additional consolidation, the deficits will cumulatively contribute to an increase in gross debt by some 17.9 p.p. of GDP. In order to stabilise the gross debt level at around 62 % of GDP, the general government deficit would need to be gradually reduced over the entire medium-term horizon until 2029, i.e. down to 2.7 % of GDP.

- As the sanction brackets of the debt brake will be declining annually to finally arrive at 50 % of GDP in 2027 (for the highest sanction bracket), the difference between the expected gross debt level and the highest sanction bracket of the debt brake will be increasing continuously. At the end of the medium-term horizon in 2029, the gross debt level would thus exceed the highest sanction bracket of the debt brake by as much as 21.4 p.p. of GDP.

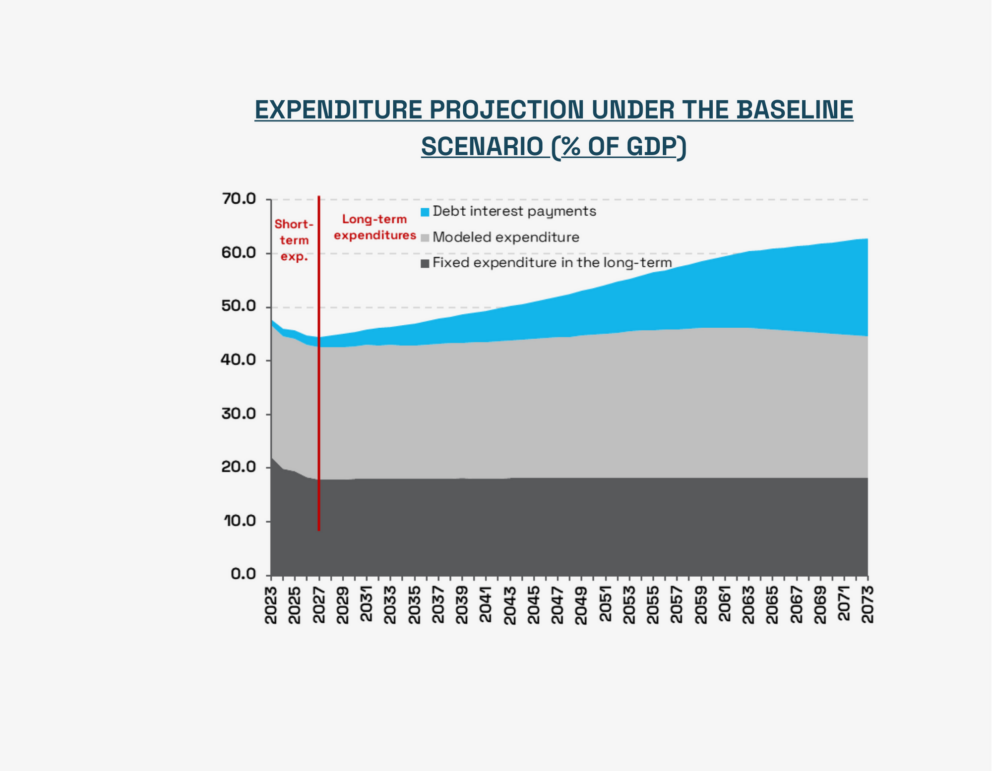

- The development in public finances under the CBR’s scenario has a negative impact on the long-term sustainability of 0.5 % of GDP compared to the situation estimated at the end of 2024. This is due to expenditure-side measures in the current year, in particular the increased indexation of wages in the school sector (0.3 % of GDP). The value of the long-term sustainability indicator would thus be shifted to 4.6 % of GDP. In order to achieve sustainability of public finances, this would require a permanent increase in revenues and/or reduction in expenditure in the amount of EUR 6.4bn.

- The CBR estimates that without continuing the consolidation of public finances after 2025, the public expenditure ceiling will not be met over the entire horizon. The mutual inconsistency between the national rule and the European rule is manifested by the fact that while the nominal expenditure ceilings assume a significantly greater need for consolidation until 2028 (EUR 5.3bn), it would be enough to put in place measures worth EUR 3.6bn when complying with the defined cumulative net expenditure growth under the European rules. Taking into account the impact of the escape clause triggered as a result of increased defence spending, measures worth EUR 2.7bn would be sufficient to comply with the European rules[7].

- As far as the new European rules are concerned, the CBR estimates that, if government expenditures were to grow in line with the mandatory path, the deficit would only decline to 4.2 % of GDP by 2027 (and to 3.4 % of GDP in 2028) while the debt would reach 66.5 % of GDP, which is significantly higher than the government’s targets. Should the deficit and debt also fully reflect the exemption allowing to increase defence spending, the deficit would only be reduced to 4.1 % GDP by 2028 while the debt would be even higher by 0.9 % of GDP compared to the CBR’s scenario, reaching 69.4 % of GDP. At the same time, the very objective of the new European rules, i.e. stabilising the debt, would not be achieved. Slovakia would therefore have to launch a new consolidation plan from 2029 after the end of this program.

- The government’s stricter deficit targets when compared to compliance with cumulative expenditure growth are based mainly on the fact that meeting the expenditure growth rate in 2024 by a large margin was not reflected in higher expenditure growth between 2025 and 2028. If the cumulative expenditure growth rates and the defence spending exemption are taken into account, a deficit higher by 1.9 % of GDP than the current estimate of the CBR would be possible in 2025. In turn, this would have an impact on subsequent years when the deficit and debt would not fall – due to the allowed high growth rates for 2024 and 2025 – below the target values of 3 % of GDP for deficit and 60 % of GDP for debt.