Summary

The Report on Compliance with the Fiscal Responsibility and Fiscal Transparency Rules annually assesses the compliance with the rules arising from the constitutional Fiscal Responsibility Act[1] for the previous year, always by 31 August. In addition to evaluating the development of the long‑term sustainability of public finances — the most important objective pursued by the act — it also assesses compliance with the constitutional debt limit, as well as other statutory obligations, especially regarding data reporting and publication, local government debt, and the funding of local governments’ competences.

Long‑term sustainability of public finances

The key objective of fiscal responsibility is to achieve sustainable public finances. The protection of long‑term sustainability of Slovakia’s economic performance regarding the compliance with the principles of transparency and effectiveness in the use of public funds, has been enshrined in the amendment to the Constitution of the Slovak Republic since 2020[2].

In its evaluation, the Council for Budget Responsibility (CBR, or Slovak abbreviation RRZ) concluded[3] that the long‑term sustainability of public finances was not achieved in 2024. Under a no‑policy‑change scenario, the long‑term sustainability indicator reached 4.1% of GDP, which means that public finances are in the medium‑risk zone. Following several measures adopted by the government and parliament[4], visible progress has been made compared to 2023 and the indicator improved year‑on‑year by 2.1 percentage points.

Taking into account the CBR’s expectations for the medium‑term development of public finances[5], as well as the measures adopted during 2025, long‑term sustainability would worsen by 0.5% of GDP compared to the estimated position at end of 2024. This reflects approved wage indexation in the education sector, higher funding for the Sport Promotion Fund and amendments to the Civil Service Act and the Employment Services Act. The CBR also expects a faster pace of wage growth for general government employees in the final year of the electoral term.

Given the persistent poor state of public finances, the government should present further ambitious measures to improve the sustainability of public finances as soon as possible. The government has declared a goal to reduce the deficit below 3% of GDP by 2028 and to halt the rise in debt[6], which is more ambitious than the current requirements under the current EU fiscal rules. According to the CBR’s current estimate and assuming the termination of energy subsidies[7], the measures needed to achieve the government’s budgetary objectives amount to €2.0 billion (1.4% of GDP) in 2026 and a further €0.9 billion (0.6% of GDP) by the end of the electoral term. Subsequently, in 2028, additional measures of €1.8 billion (1.2% of GDP) will be required due to the expiration of temporary consolidation measures in 2027 (in particular the increased rate of health contributions and the increased regulated levy on banks).

The size of the consolidation package required is also affected by the fact that, at the end of 2023 and 2024, the government and the parliament approved measures that increase expenditure and reduce revenue (for example, raising the 13th pension payments, higher spending in healthcare, a reduced 5% VAT rate for selected goods and services, or a lower corporate income tax rate for small firms). Provided that these measures were not introduced and the consolidation measures were permanent in their full size, budgetary goals would have been met until 2027 without a need for further consolidation and for 2028, the need for consolidation measures would reach €1.7 billion (1.0% of GDP)[8].

The need to continue improving long‑term sustainability is further amplified by the currently high level of gross debt, which has now been in the highest sanction bracket of the debt‑brake mechanism for the fifth consecutive year. Without additional consolidation measures with the potential to noticeably improve the structural balance going forward, the current level of debt will pose an increasing risk to the sustainability of public finances.

Fiscal responsibility rules

To achieve long‑term sustainability of public finances, the constitutional act sets out fiscal responsibility rules. The operational and counter‑cyclical instrument of budget management should be the expenditure ceilings. The general government debt limit (the so‑called debt brake) should prevent debt from persistently exceeding levels that may be regarded as excessive. However, the CBR’s recommendations to strengthen fiscal responsibility have repeatedly not been implemented.

The way the constitutional act is currently applied and followed[9] by governments and the parliament has failed to provide sufficient safeguards for long‑term sustainability, in particular due to the absence of effective expenditure ceilings and the merely formal approach to complying with the debt‑brake sanctions. The constitutional act should therefore be modernised so that it reflects current debt developments, the need for effective liquidity management and, above all, so that the debt brake becomes an effective instrument for improving long‑term sustainability (for example, by introducing stricter measures when lower sanction brackets are exceeded and by protecting the economy from an abrupt change in fiscal policy, provided sufficient consolidation has been achieved). This requires a cross‑party consensus. At the same time, the debt brake is disproportionately strict for local governments, which have minimal scope to contribute to a reduction in overall public debt[10].

An amendment to the constitutional act is also necessary to ensure alignment of national legislation with the European framework. As part of the reform of the EU fiscal framework, principles on the independence and minimum tasks of fiscal councils in the EU were adopted. Slovakia should transpose these changes[11] into national legislation by the end of 2025.

An essential precondition for effectively safeguarding long‑term sustainability is a change in the approach of governments and the parliament to the fiscal responsibility rules. A formal approach which circumvents the purpose of the rules must be replaced by genuine compliance. Merely tightening the debt‑brake sanctions or refining the wording of the constitutional act may be insufficient if there is no functioning mechanism to ensure compliance with its provisions. The European expenditure rules set justified minimum guardrails, but they do not necessarily provide optimal guidance for economic policy once all of Slovakia’s needs are taken into account. It would therefore be appropriate to re‑link the public expenditure ceilings to the long‑term sustainability indicator under the constitutional act, as was the case under the original national expenditure ceilings in force from late 2022 to July 2024. This would better ensure the improvement required in the long‑term health of public finances.

General government debt limit

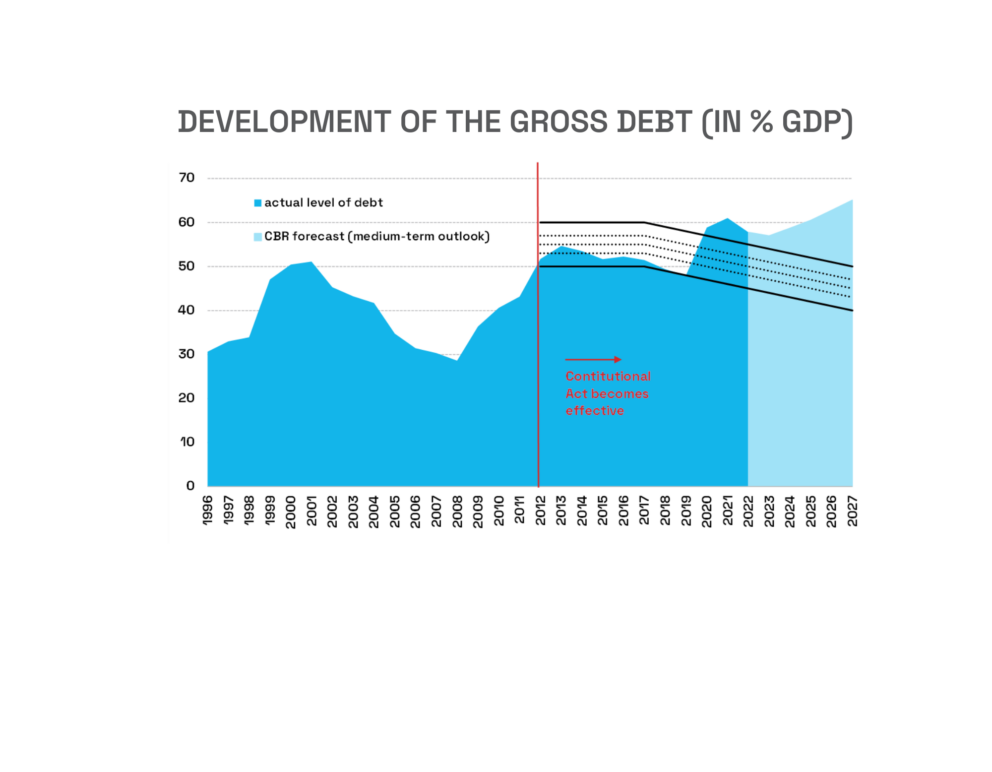

The debt‑to‑GDP ratio remained in the highest, fifth sanction bracket[12] of the debt‑brake mechanism in 2023 and 2024. Based on data published by Eurostat in October 2024, the debt stood at 56.1% of GDP at the end of 2023, and according to preliminary data[13] released in April 2025 it reached 59.3% of GDP at the end of 2024.

Because the 24‑month exemption from the application of stricter sanctions under the constitutional act[14] has been in effect since 22 November 2023, the level of debt achieved in 2023 was subject to the sanctions triggered by the first and second sanction brackets of the constitutional Fiscal Responsibility Act (Table 1).

Due to the duration of the 24‑month exemption until (and including) 21 November 2025, the debt level achieved in 2024 is associated with the sanctions applicable to the first two sanction brackets of the debt‑brake mechanism. From 22 November 2025, the debt level will be associated with the sanctions resulting from all five sanction brackets of the constitutional Fiscal Responsibility Act[15] (Table 2). The assessment of the sanctions triggered by exceeding the third, fourth and fifth sanction brackets will only be possible after the exemption expires or, as appropriate, after the end of the year.

Despite the high levels of general government debt, which has continuously remained in the highest sanction bracket of the debt‑brake mechanism since 2020, compliance with the sanctions has in recent periods been only formal and has had a minimal effect in reducing the general government debt. Examples include the repeated submission[16] of proposals to reduce the debt which typically lack a sufficient set of concrete measures, the blocking of 3% of state‑budget expenditures in May 2023 without affecting the general government balance, or the merely formal proposal for a balanced general government budget for 2024–2026 which, according to the government’s own statement, would have caused a recession and jeopardised the functioning of the state.

According to the authors of the constitutional Fiscal Responsibility Act, the implementation of measures triggered by exceeding the debt‑brake sanction brackets should lead to a reduction of the state’s indebtedness to a safe level. In practice, however, the measures adopted by successive governments have long failed to meet this objective. Experience has shown that governments are unwilling to truly comply with the constitutional act and regularly circumvent the debt‑brake sanctions, thereby ignoring the purpose of the act, namely the achievement of long‑term sustainable public finances of the Slovak Republic.

The Slovak Republic — that is, all its bodies of state power and public authority — is obliged to protect the long‑term sustainability of the country’s public finances. If the fiscal position is not sustainable in the long term, a situation may arise in which the state will not be able to properly ensure the protection of fundamental rights in the future, in particular those that depend on public funding[17]. When preparing the general government budget proposal and measures to safeguard long‑term sustainability, the government enjoys a margin of discretion only within the limits set by generally binding legislation[18]. Formalism in the interpretation and application of the relevant constitutional norms is inadmissible. Formal compliance with the constitutional act without fulfilling its purpose may be deemed a violation thereof[19].

In the medium term, the CBR estimates[20] that without additional consolidation measures, gross debt will increase cumulatively by 15.5 p.p., from 59.3% of GDP at end of 2024 to 74.8% of GDP in 2029. The projected increase in general government debt is mainly driven by a very unfavourable development in the structural primary balance. The highest sanction bracket of the debt brake will start at 50% of GDP in 2029, which would imply an exceedance by 24.8 p.p.

Public expenditure ceilings

From the outset, in addition to the debt limit, the constitutional act envisaged the introduction of expenditure ceilings as an operative budget management tool and an imperative component of responsible fiscal policy. However, the public expenditure ceilings were only enacted eleven years after the adoption of the constitutional act. With effect from 1 April 2022, they became the main budgetary instrument for achieving the long‑term sustainability of public finances under the constitutional act, but they only remained in force in that form only until 31 July 2024. With effect from 1 August 2024 the public expenditure ceiling has been linked solely to the reformed EU rules under the Stability and Growth Pact.

The Ministry of Finance justified the change in the rules for setting the public‑expenditure ceiling by the need to eliminate inconsistencies between the national and the European fiscal frameworks; according to the CBR, this has not been achieved. The nominally defined ceiling (the national rule) does not respond to revisions in national accounts, nor to the changed effects of adopted revenue measures. It sets the expenditure limit for a given year without considering its fulfilment in previous years. On the other hand, the net expenditure growth (European rule) does not contain these shortcomings and primarily considers the cumulative path of expenditure growth over a multi-year period[21]. Whereas the nominally set ceilings do not provide explicit constraints if the national defence escape clause is activated[22], under the European rule the maximum amount by which the ceiling may be exceeded is specified[23].

Already in last year’s report the CBR warned that the approved changes to the functioning of the ceiling are likely inconsistent with the concept of safeguarding the long‑term sustainability of the Slovak Republic enshrined in Article 55a of the Constitution and in the constitutional Fiscal Responsibility Act. They can be regarded as a significant weakening of the previous framework of rules because expenditure ceilings linked only to European rules do not sufficiently[24] reflect the need to achieve long‑term sustainability over a 50‑year horizon.

Linking the public expenditure ceiling to the European rules may lead to a slower and more delayed permanent recovery of public finances[25]. In Slovakia’s case, the set trajectory for the growth of net expenditures is based on optimistic assumptions[26], which means that the required net‑expenditure growth rates are too loose and will not deliver the necessary consolidation. Moreover, the application of the defence ‘escape clause’ can further relax the framework by allowing higher defence spending at the expense of a higher deficit and debt[27]. In addition, the rule may not be sufficiently functional or flexible; its correction mechanism is likely to be lengthy in the event of non‑compliance, it will be less precise against potential circumvention and more rigid in times of crisis.

Specific provisions for local government

The rules applicable to the local government sector aim to separate the responsibility for the solvency of local governments from the state, to ensure that their new tasks are financed by the state and to prevent excessive indebtedness on the part of local governments. For these reasons, the following three areas are evaluated: (1) whether the state has abstained from providing funds to ensure local‑government solvency; (2) whether new tasks and competences have been devolved to local government without adequate financial coverage; and (3) the level of local government debt.

- Based on the information currently available, it can be stated that in 2024 the state did not participate financially in ensuring the solvency of local governments, which is consistent with the requirement of the constitutional act to ensure budgetary discipline and the clear allocation of responsibility for the exercise of local‑government powers. During 2024 the government did not provide repayable financial assistance to local governments from the state’s financial assets. However, through the partial remission of repayable financial assistance and the provision of direct grants it improved the financial position of local governments[28]. The current rules for the provision of repayable financial assistance from the state’s financial assets should be amended to prevent the selective favouring of local governments and to avert future insolvency.

- Based on the information currently known, in the course of 2024 the amendments to the Construction Act and the Spatial Planning Act created new tasks for local governments in both their own competences and in their delegated performance of state administration, which required financing to be provided by the state[29]. Given the scope of changes in construction legislation, changes in the related administrative fees and the fact that the state introduced new forms of administrative fees during 2025, it is not currently possible to unambiguously assess whether the financing of these new tasks is adequate. Associations representing local governments point to the risk that the new tasks may necessitate increased staffing and higher funding needs. On the other hand, higher revenues from fees may cover these costs.

In line with the principles of transparency and effectiveness, any changes relating to the financing of local governments must always be subject to a standard consultation procedure and be costed explicitly. It is also necessary to consistently respect and monitor the impacts of measures so that central government authorities do not impose additional burdens on local government budgets without identifying them in the impact clauses and, at the same time, to prevent the transfer of new tasks (whether in the exercise of original or delegated local government powers) to local governments without adequate financial coverage.

- In the case of local governments with excessive debt[30], the administrative proceedings on the imposition of fines for 2023 were completed. While all self‑governing regions ended up below the statutory debt limit, out of 30 initially identified municipalities, after taking legislative exemptions into account and verifying the reported figures, fines were imposed on two municipalities. For 2024, 23 municipalities are preliminarily at risk to receive a fine; the verification of the reported figures is ongoing. Further 27 municipalities were contacted because they had not submitted the required financial statements. All self‑governing regions also remained below the statutory debt limit in 2024. The Ministry of Finance assessed compliance with the local‑government debt rule, with the possibility to impose a fine, for the first time for 2015, but has not yet published a single evaluation. The CBR recommends that the Ministry of Finance transparently disclose[31] all information related to verifying the level of local‑government debt and the imposition of fines.

Fiscal transparency rules

The fiscal transparency rules defined by the constitutional act were almost fully complied with. Macroeconomic and tax revenue forecasts were approved by the competent independent committees and published within the deadlines set by the constitutional act. The 2025–2027 general government budget contained all the data required by law, with the exception of information on a majority of companies with the participation of the Ministry of Health of the Slovak Republic (health‑care facilities and Všeobecná zdravotná poisťovňa). The annual summary report for 2023 contained all the data required by law.

In addition to the requirements defined by law, the CBR also assesses the budget transparency in terms of comprehensibility and quality of the information contained in the assessed documents, consistent application of the ESA2010 methodology, and the degree of parliamentary control over the approval and execution of the budget. These were also the focus of the CBR’s recommendations in the August 2024 report, in which no progress has been made. On the contrary, transparency decreased in relation to achieving the budget target for 2025 due to non‑use of the ESA 2010 methodology for energy subsidies[32], and parliamentary and public oversight over those state budget expenditures that used to be treated as reserves has also weakened.

Among the main persisting shortcomings, the remedy of which could improve fiscal transparency and the entire budgetary process, the CBR highlights:

- The general government budget was aligned with the budgetary objectives only for 2025. To meet the objectives in 2026 and 2027, the budget lacked specific measures amounting to 0.4% and 1.9% of GDP, respectively. The amended public expenditure ceilings, linked to the reformed European fiscal rules and evaluated only for the following year, have not increased the binding nature of preparing a three‑year budget.

- The CBR repeatedly notes that the current legislative framework for the approval of the budget in the National Council of the Slovak Republic is not adequate in terms of the subject‑matter and content of the documents being approved. The parliament’s approval of a (cash‑based) state budget for the next year is rooted in historical practice and is no longer sufficient to capture the key monitored parameters of public finances and all changes in public finances, in line with European standards defined by the ESA 2010 methodology.

- The expenditure side of the budget should be based to a much greater extent on a no‑policy‑change scenario for the following three years, as required in the past by the Act on the General Government Budgetary Rules[33]. In recent years this approach has been used only for the budgeting of health‑insurance companies’ expenditures, which allowed a transparent assessment of the assumptions underlying the health‑sector budget, including the impacts of the incorporated measures. The 2025–2027 general government budget did not include such information even for health‑care expenditures[34].

- Information on state‑owned enterprises should be improved. A short commentary on the expected economic results of individual enterprises would allow better assessment of potential risks arising from the performance of enterprises owned by the state, or by MH Manažment, a.s.

- The information value of the net‑worth indicator could be enhanced by valuing the as‑yet unquantified components of net worth, which the Ministry of Finance is currently working on[35]. For a deeper analysis of the impact of government measures on net worth, it is necessary to create the technical prerequisites for data collection and, in co‑operation with the CBR, to define a methodology linking the change in net worth to the budget balance.