Find the complete analytical material, including the Appendix and the data file, in the download section below the article.

Assessment of Compliance with Expenditure Ceilings in 2025

Pursuant to obligations arising from Section 30(4) of Act No. 523/2004 Coll. on General Government Budgetary Rules (hereinafter the “Act”), the Council for Budget Responsibility (CBR) assesses compliance of the budgetary outturn with the net expenditure path (the Stability and Growth Pact rule) and with the public expenditure ceiling (the national rule). At the same time, it publishes an analysis of the factors explaining deviations from the net expenditure path.

The CBR assessment is based on data for 2023–2025 from the spring deficit and debt notification published by the Statistical Office of the Slovak Republic on 21 April 2026, supplemented by the CBR’s own estimates of cyclical unemployment benefit expenditure and the impact of discretionary revenue measures.

Incorrect initial calibration of the rules causes the ineffectiveness of expenditure ceilings in Slovakia

The reformed Stability and Growth Pact (EU fiscal rules) was intended to enable countries to reduce deficits and debt in a sustainable and realistic manner through control of expenditure growth. Its objective was to stabilise public debt below 60% of GDP. Although this framework appears to be clearly defined at first glance, in the case of Slovakia, its initial calibration was flawed[1], as also pointed out by the CBR.

Under the applicable rules, the Ministry of Finance of the Slovak Republic (MF SR) was the only entity authorised to request correction of this flawed initial calibration. Unlike several other EU Member States, however, the MF SR did not take such action. As a result of the passive approach of the MF SR in setting the rules[2], the current EU fiscal rules now allow, according to the latest estimates, the achievement of a general government deficit of approximately 5.4% of GDP and public debt of 73.3% of GDP by the end of 2028.

This implies that in Slovakia’s case, mere compliance with EU rules would not be sufficient to ensure long-term sustainability of public finances. Since the national expenditure rule is derived from the EU fiscal rule, its functioning is likewise affected by this flawed initial calibration. Assessment of compliance with both rules therefore needs to be interpreted in this context.

Growth of net expenditure in 2024 and 2025 (Stability and Growth Pact rule)

On 21 January 2025, the Council of the European Union approved Slovakia’s national medium-term fiscal-structural plan, including the maximum growth rate of net expenditure for individual years during 2025–2028 and the cumulative growth rate of net expenditure in 2028 compared to 2023 (Table 1). In 2025, the rule allowed a cumulative growth in net expenditure of 10.3%.

Subsequently, on 8 July 2025, the Council of the European Union approved activation of the national escape clause for the Slovak Republic, whereby the exemption allows defence expenditure in 2025–2028 to increase by up to 1.5% of GDP relative to the 2021 level without being included in expenditure subject to the ceiling[3].

Subsequently, on 8 July 2025, the Council of the European Union approved activation of the national escape clause for the Slovak Republic, whereby the exemption allows defence expenditure in 2025–2028 to increase by up to 1.5% of GDP relative to the 2021 level without being included in expenditure subject to the ceiling[3].

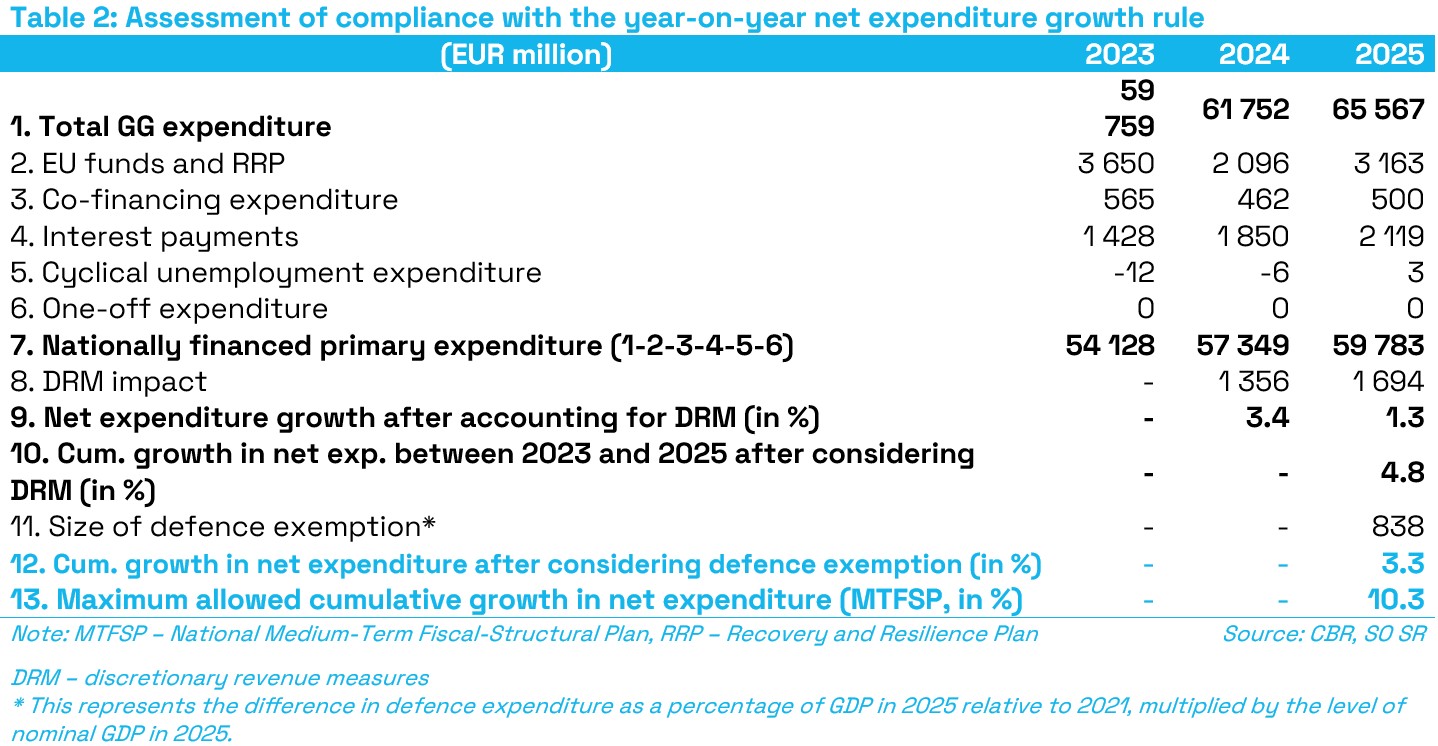

When assessing compliance of the budgetary outturn with the net expenditure path, the CBR proceeded according to the definition of maximum net expenditure growth under the EU fiscal rules, whereby expenditure financed from the EU budget, co-financing, interest costs, cyclical unemployment expenditure and one-off impacts are deducted from total general government expenditure. Subsequently, after calculating the growth rate of net expenditure incorporating the effect of discretionary revenue measures, the impact of the defence exemption is also deducted. The CBR assesses compliance with the rule on a cumulative basis, which is fully consistent with the approach of the European Commission, which will assess the rule cumulatively in countries with an active national defence escape clause[4].

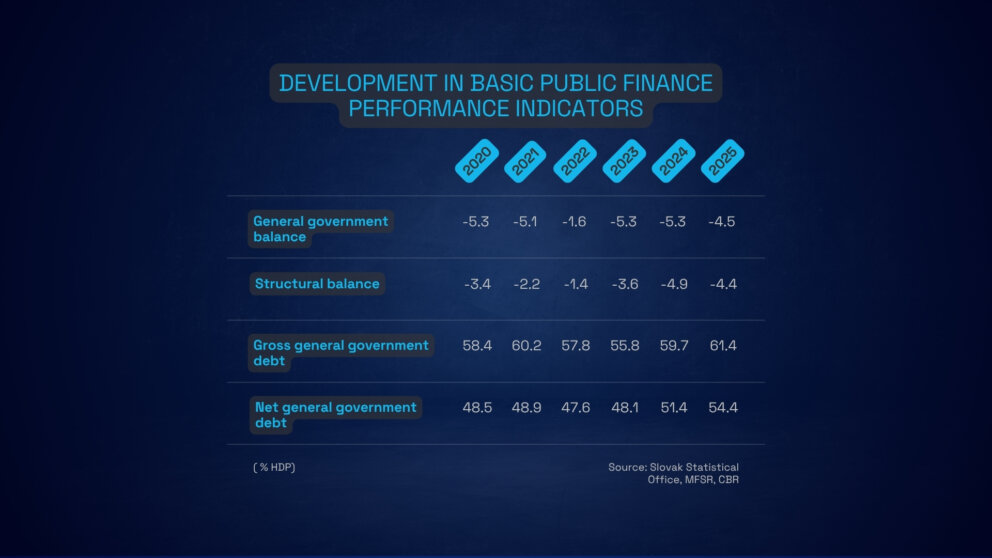

The CBR concludes that the net expenditure growth in 2025 (without applying the defence exemption) reached 1.3% year-on-year, which is 2.6 percentage points below the approved trajectory. Cumulative growth in net expenditure for 2024 and 2025, after inclusion of the defence exemption, reached 3.3%, thereby meeting the rule with a margin of 7.0 percentage points[5] (Table 2). Such compliance with the rule is partly influenced by the government’s consolidation measures approved at the end of 2023 and 2024, which increased revenues (thereby also increasing room for expenditure growth), as well as by factors outside the government’s control (decline in energy subsidies due to falling energy prices). To a large extent, however, it is mainly the consequence of incorrectly calibrated rules for Slovakia[6], since using the maximum room for expenditure growth allowed by the rule would have enabled the general government deficit to reach as high as 7.3% of GDP in 2025[7]. This is inconsistent with the main objective of the rule – to sustainably reduce the deficit below 3% of GDP and debt below 60% of GDP.

Despite formal compliance with the rules, the development of public finances is significantly more negative than the original projected trajectory of deficit and debt by the European Commission. The Commission originally projected that compliance with the expenditure rule targets would stabilise debt and expected a deficit of 1.7% of GDP and debt of 61% of GDP in 2028. Currently, under compliance with the rules, the CBR estimates a deficit of 5.4% of GDP[8] and debt of 73.3% of GDP in 2028.

Despite formal compliance with the rules, the development of public finances is significantly more negative than the original projected trajectory of deficit and debt by the European Commission. The Commission originally projected that compliance with the expenditure rule targets would stabilise debt and expected a deficit of 1.7% of GDP and debt of 61% of GDP in 2028. Currently, under compliance with the rules, the CBR estimates a deficit of 5.4% of GDP[8] and debt of 73.3% of GDP in 2028.

Analysis of factors explaining deviations from the net expenditure trajectory

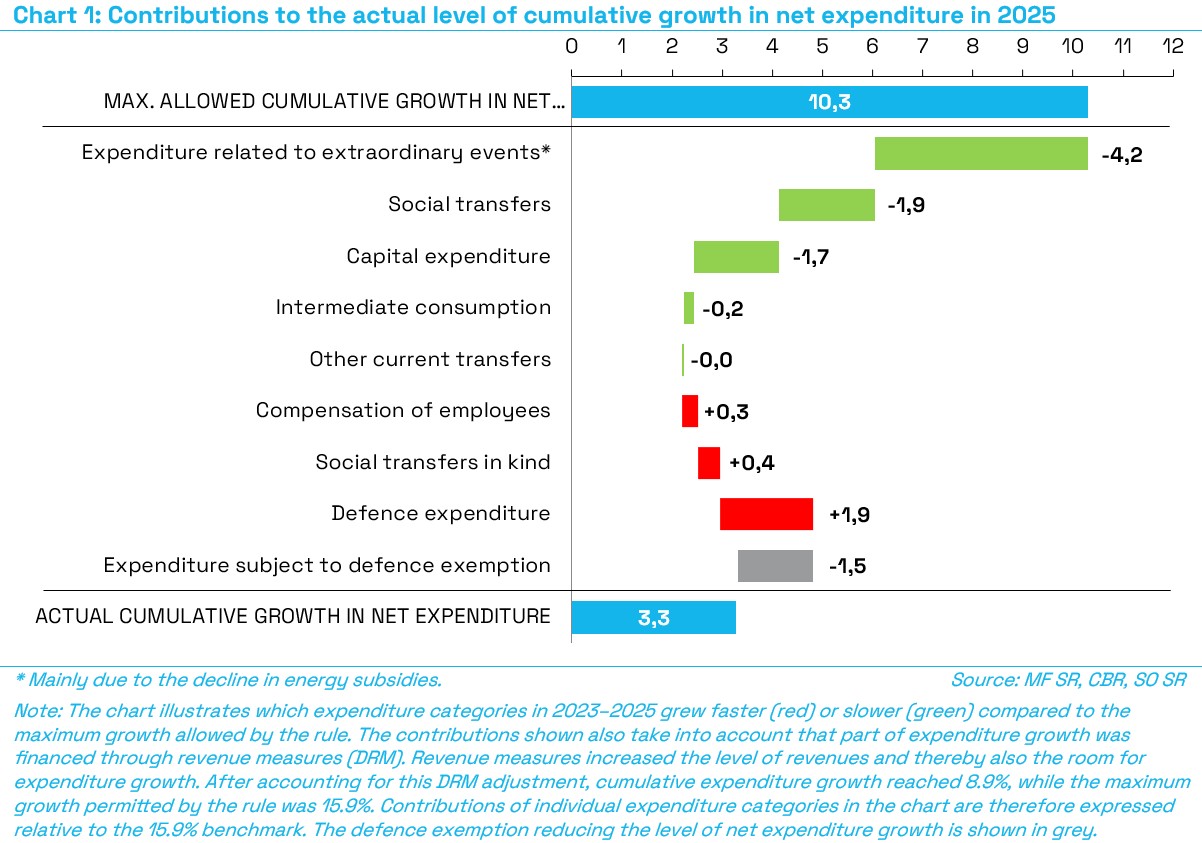

By comparing the cumulative year-on-year development of individual expenditure categories (adjusted for the impact of EU funds, co-financing, interest costs and the economic cycle) with the maximum cumulative growth in net expenditure, the CBR calculated their contributions to the total deviation (Chart 1).

The lower pace of growth in net expenditure was driven mainly by the substantial decline in expenditure related to extraordinary events, particularly energy subsidies, which recorded the sharpest decrease since 2023 (contribution of 4.2 percentage points). From the perspective of cumulative compliance with this expenditure rule, this only formally represents a permanent saving[9], provided that expenditure on energy subsidies does not return to the high levels seen in 2023. The reason is that this does not represent an active saving resulting from government policy, but merely reflects the natural decline in market prices from the extreme levels observed in 2023. A significant contribution also came from the decline in social transfers in 2025 (1.9 percentage points), mainly reflecting the reduction in the child tax credit approved back in 2022[10], as well as lower expenditure on sickness benefits and parental allowance in 2025. Investments outside the defence sector declined compared to 2023 (contribution of 1.7 percentage points).

On the other hand, expenditure on healthcare provided by health insurance companies (0.4 percentage points) and compensation of employees (0.3 percentage points) grew more rapidly, primarily reflecting wage indexation. However, the most pronounced increase in expenditure occurred in the defence sector (1.9 percentage points), mainly due to deliveries of military equipment in 2025. Given the defence exemption, however, the overall negative impact of defence amounted to only 0.4 percentage points.

Public expenditure ceiling for 2025 (national rule)

The nominal value of the public expenditure ceiling for 2025 was calculated by the MF SR based on the recommendation of the Council of the European Union, according to which growth in net primary expenditure in 2025 compared to 2024 should not exceed 3.8%. The same set of expenditure items fell under the public expenditure ceiling as under the definition of net primary expenditure in the reformed Stability and Growth Pact rules[11].

The public expenditure ceiling for 2025 was approved together with the general government budget for 2025-2027 on 3 December 2024, and its value was set at EUR 61,143,359,188. According to the CBR, the ceiling was met with a margin of EUR 1.4 billion (Table 3). If the assessment of the ceiling also incorporated differences in the estimate of discretionary revenue measures (DRM) compared to their value used in calculating the ceiling, and reflected the approved national defence escape clause allowing the established ceiling to be exceeded[12], the ceiling would have been met by EUR 2.1 billion.

Since the nominally determined ceiling serves for operational budget management[13] and is linked to the net expenditure growth rule under the Stability and Growth Pact, it is important for these rules to be mutually consistent. This is currently not the case, since under the nominally determined ceiling the deficit in 2025 could reach a maximum of 6.0% of GDP, while the EU rule allowed a deficit of as much as 7.3% of GDP. The main reason is the annual horizon of the national rule, since unlike the EU rule assessed cumulatively over several years, it does not take into account the degree of compliance with the ceiling in previous years. At the same time, the level of the nominally determined ceiling does not flexibly reflect changes in assumptions on the basis of which it was calculated[14]. This mainly concerns changes in reported expenditure for the previous year and changes in the estimated impact of discretionary revenue measures.