Rozpočet verejnej správy na roky 2024 až 2026 je prvý rozpočet predložený vládou, ktorá vzišla z parlamentných volieb konaných v septembri 2023. Vzhľadom na neskorý termín konania volieb ako aj rozhodnutie vlády prijať rozpočet do konca roka, bol návrh rozpočtu schválený vládou 12. decembra 2023. V nadväznosti na to Národná rada SR schválila zákon o štátnom rozpočte 21. decembra 2023.

Pozrite si: Hlavné závery hodnotenia

Objektívne treba skonštatovať, že súčasná vláda prevzala verejné financie po dvoch krízach v komplikovanom stave, čo znamená, že bez opatrení vlády by sa deficit pohyboval v rokoch 2024 až 2027 na úrovni 6 % HDP a dlh Slovenska by postupne narastal k hranici takmer 70 % HDP. Verejné financie sa pohybujú v pásme vysokého rizika dlhodobej udržateľnosti. Podľa odhadov Rady aktuálny zlý stav verejných financií bol ovplyvnený hlavne bezpečnostnou a ekonomickou krízou a pandémiou, počiatočným vysokým štrukturálnym deficitom na konci dobrých ekonomických časov, ako aj opatreniami prijatými v roku 2023. Posledné dva dôvody vznikli aj ako dôsledok chýbajúcej (resp. v roku 2023 pozastavenej) implementácie limitov výdavkov, ako hlavného nástroja na riadenie rozpočtu a zlepšovanie dlhodobej udržateľnosti.

Oproti pôvodne rozpočtovanému deficitu verejnej správy v roku 2023 na úrovni 6,4 % HDP vláda aktuálne odhaduje nárast schodku na úroveň 6,5 % HDP. V roku 2024 návrh rozpočtu predpokladá medziročné zlepšenie deficitu na úroveň 6,0 % HDP. Schválený rozpočet predpokladá postupné zníženie deficitu k úrovni 5,6 % HDP do roku 2026. Vláda deklaruje zámer dosiahnutia deficitu verejnej správy vo výške 5,0 % HDP v roku 2025 a následne vo výške 4,0 % HDP 2026, pričom v súčasnosti nemá pre tieto roky pripravené opatrenia.

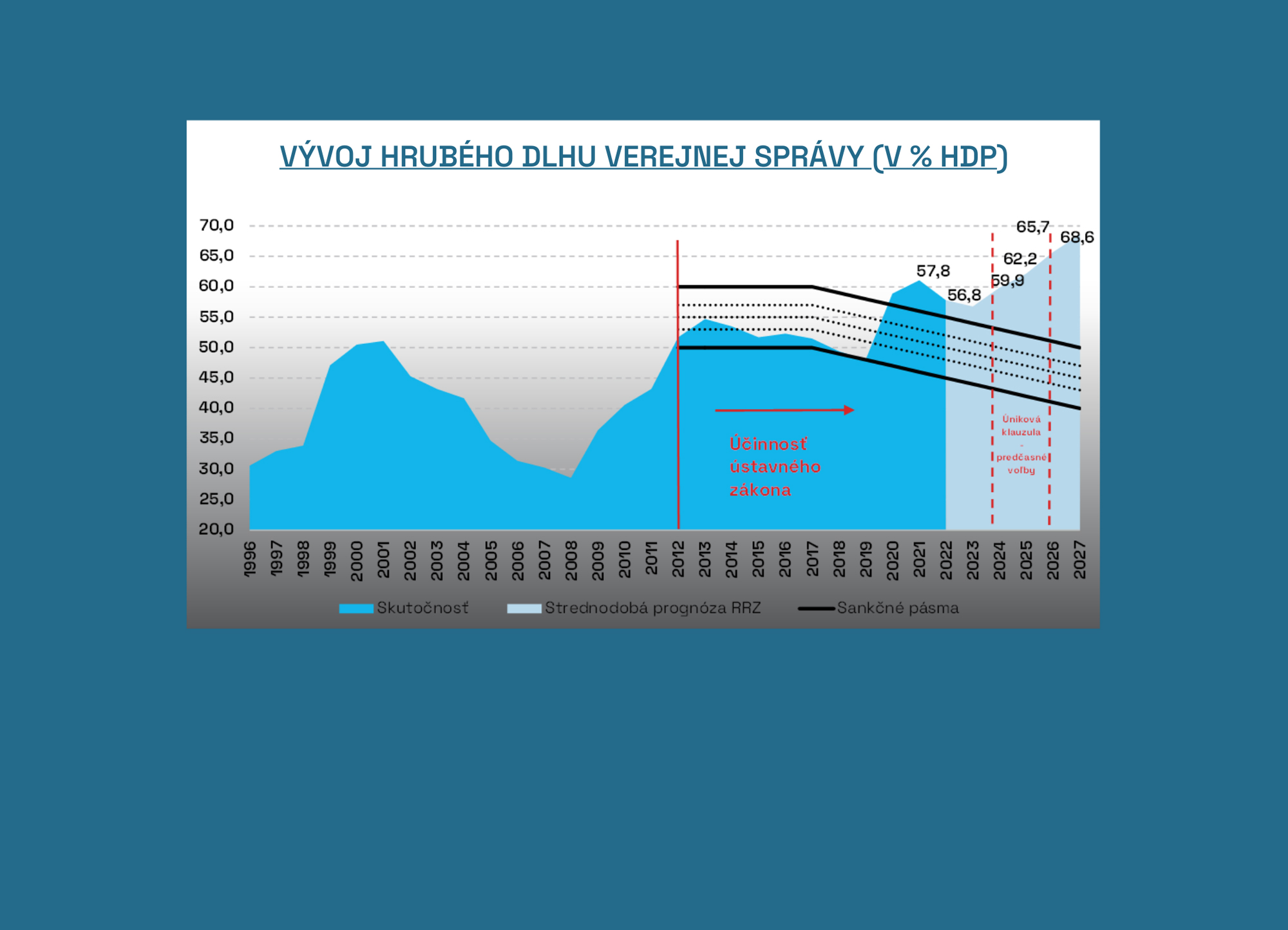

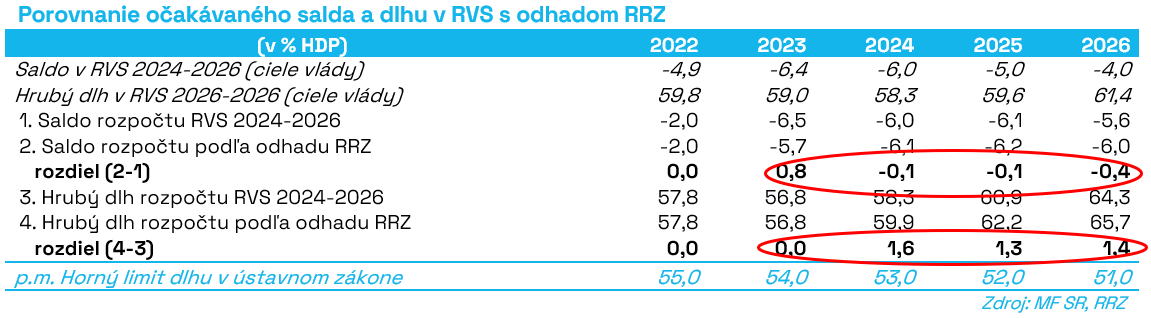

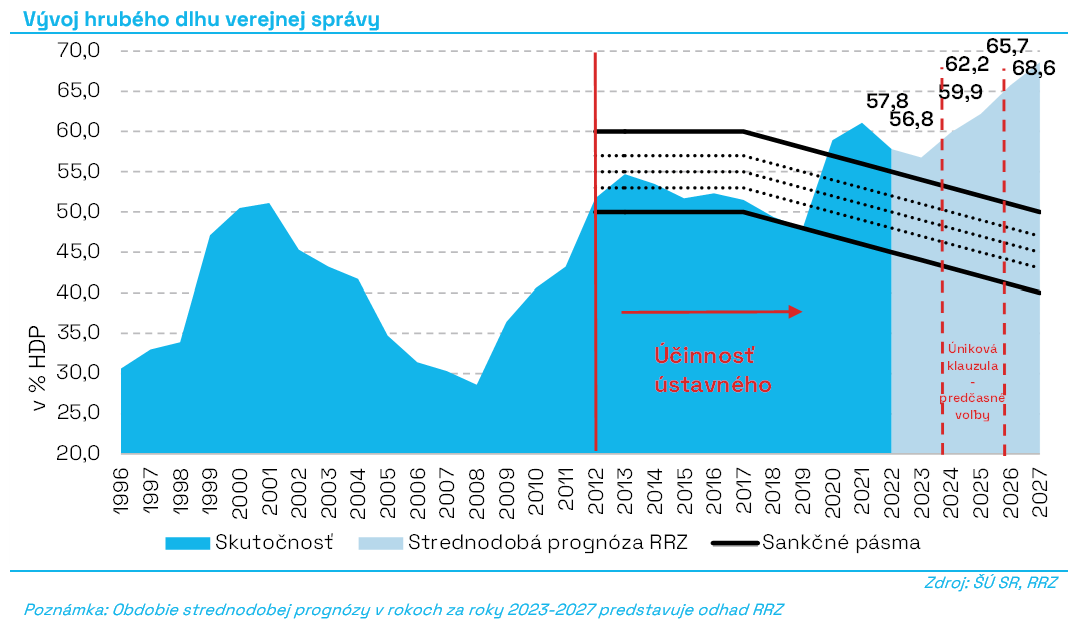

Rozpočet by podľa vlády mal viesť k poklesu hrubého dlhu z úrovne 57,8 % HDP v roku 2022 na úroveň 56,8 % HDP v roku 2023 a následne k postupnému nárastu k úrovni 61,4 % HDP na konci roku 2026 za predpokladu splnenia opatreniami nepodložených rozpočtových cieľov. Nárast je spôsobený najmä vysokými úrovňami deficitov očakávaných v najbližšom období. Bez ohľadu na predpokladaný vývoj dlhu platí, že počnúc rokom 2020 dlh prekročil horný limit sankčných pásiem ústavného zákona a podľa MF SR nad týmto limitom zotrvá počas celého prognózovaného obdobia.

Návrh rozpočtu nebol zostavovaný v súlade s výdavkovými limitmi, pričom vláda argumentuje, že v čase prípravy a schvaľovania rozpočtu neexistovali žiadne platné limity. Vzhľadom na to, že podľa RRZ v súčasnosti platia limity schválené NR SR dňa 1. februára 2023 až kým NR SR neschváli nové, RRZ pripravila porovnanie rozpočtu s limitmi verejných výdavkov.

RRZ dňa 15. decembra 2023 predložila do NR SR limity verejných výdavkov na roky 2024 až 2027 vypočítané na základe stavu legislatívy na začiatku funkčného obdobia novej vlády, aby férovo zohľadnili zdedený legislatívny stav ku dňu schváleného programového vyhlásenia vlády. Limity na roky 2024 až 2027 by po schválení Národnou radou nahradili doteraz platné limity z februára 2023, napriek tomu doteraz neprišlo k ich prerokovaniu a schváleniu NR SR.

Z dôvodu porovnateľnosti so schváleným rozpočtom Rada pripravila predbežný výpočet[1], ako by vyzerali limity verejných výdavkov po zohľadnení všetkých legislatívnych zmien, ktoré ovplyvňujú príjmy alebo dlhodobú udržateľnosť verejných financií, prijatých v NR SR v decembri 2023. Po zohľadnení týchto opatrení schválený rozpočet verejnej správy prekračuje výdavkové limity o 1,7 mld. eur v roku 2024 a následne o 2,2 mld. eur v roku 2025 a 2 mld. eur v roku 2026[2]. Keďže limity verejných výdavkov vyžadujú každoročné zlepšovanie dlhodobej udržateľnosti o 0,5 % HDP ročne a zároveň samotné MF SR priznáva, že sa udržateľnosť nezlepšuje, rozpočet nemôže byť v súlade s výdavkovými limitmi ani podľa MF SR. Odchýlka rozpočtu od limitu v roku 2024 znamená, že naplnenie rozpočtu v oblasti výdavkov spadajúcich pod limit zhoršuje dlhodobú udržateľnosť až o 0,8 % HDP.

Rozpočet verejnej správy na roky 2024 až 2026 tak nebol zostavený v súlade s výdavkovými limitmi[3] a takýto rozpočet neobsahujúci limity verejných výdavkov bol schválený národnou radou. Rozpočet preto nespĺňa ustanovenia § 30aa ods. 8 zákona č. 523/2004 o rozpočtových pravidlách verejnej správy, podľa ktorých je vláda povinná zosúladiť návrh rozpočtu verejnej správy s platným limitom verejných výdavkov. Keďže limit verejných výdavkov je hlavným rozpočtovým nástrojom na dosiahnutie dlhodobej udržateľnosti verejných financií, jeho opomenutím v rozpočte môže dochádzať k porušeniu čl. 55a Ústavy SR, v ktorej sa Slovenská republika zaväzuje chrániť dlhodobú udržateľnosť svojho hospodárenia, ako aj čl. 7 ods. 3 ústavného zákona č. 493/2011, ktorý stanovuje požiadavku určenia limitu verejných výdavkov, a to nielen ako formálnu existenciu limitu, ale aj potrebu jeho implementácie v rozpočtovom procese[4].

Cieľom stanovísk Rady pre rozpočtovú zodpovednosť (RRZ, Rada) je poskytnúť nezávislý pohľad na rozpočet a posúdiť, či je aktuálne nastavenie fiškálnej politiky postačujúce na dosiahnutie stanovených cieľov a identifikovať prípadné riziká, ktoré by bolo nutné následne dodatočnými opatreniami eliminovať. V súlade so svojim mandátom RRZ poukazuje aj na to, či aktuálny rozpočet vytvára predpoklady pre zabezpečenie dlhodobej udržateľnosti verejných financií a plnenie národných fiškálnych pravidiel. S týmto cieľom RRZ poukazuje na nasledujúce hlavné závery svojho hodnotenia:

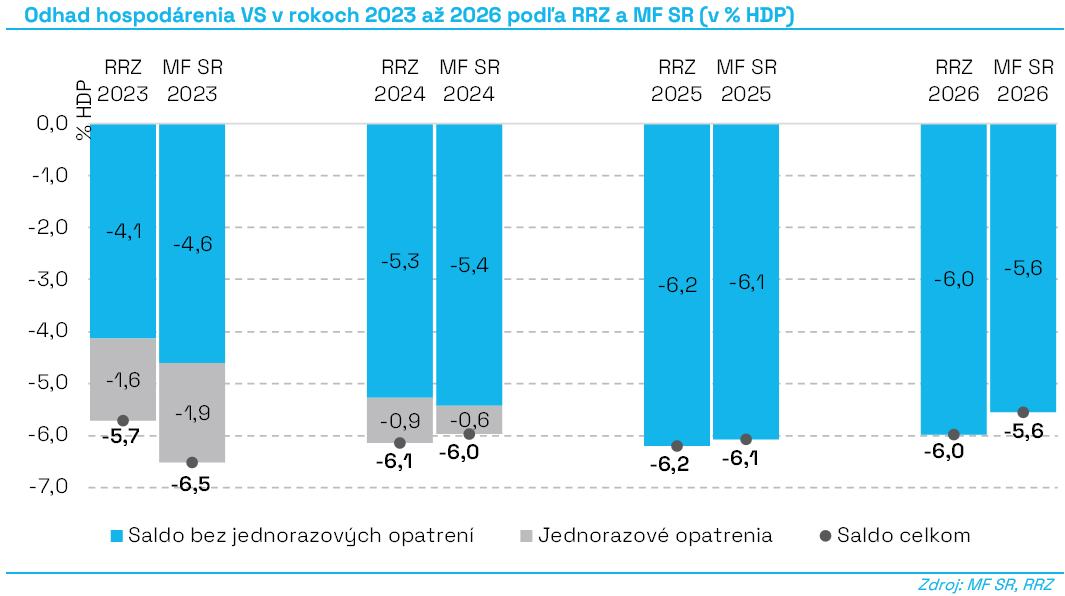

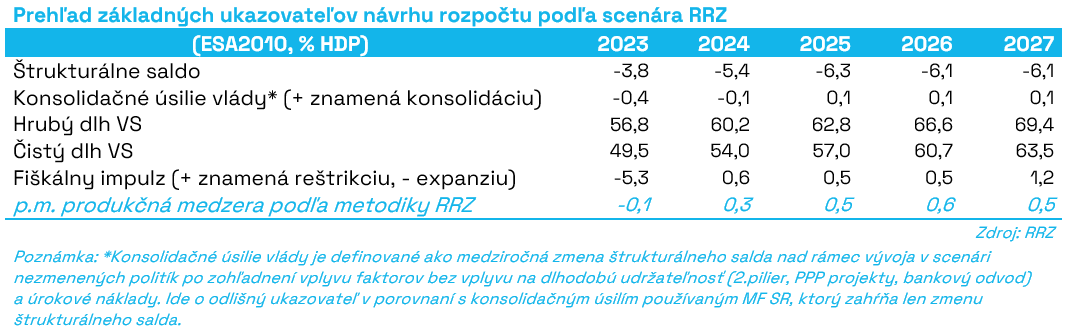

- Rok 2023 je východiskovým rokom pre zostavenie Rozpočtu verejnej správy na roky 2024 až 2026. Na základe aktuálnych informácií vrátane výsledku hotovostného hospodárenia štátneho rozpočtu môže deficit v roku 2023 podľa Rady dosiahnuť len 5,7 % HDP. V porovnaní s aktuálnym odhadom vlády to predstavuje výrazne lepšiu východiskovú pozíciu (o 0,8 % HDP) pre obdobie rokov 2024 až 2026. Pozitívna odchýlka súvisí najmä s nezohľadnením EÚ refundácií pre energokompenzácie v plnej miere v odhade vlády ako aj s nadhodnotením kapitálových výdavkov štátneho rozpočtu oproti aktuálnemu vývoju.

- V scenári nezmenených politík (bez nových opatrení schválených vládou zostavenou po parlamentných voľbách) by deficit VS z úrovne 5,4 % HDP v roku 2023 vzrástol na úroveň 5,6 % HDP v roku 2024 a následne v rokoch 2025 až 2027 výraznejšie na hodnoty v rozmedzí 6,3 % HDP až 6,5 % HDP. V rámci rokov dochádza k posunom vplyvu vysokej inflácie na verejné financie, keďže na rozdiel od príjmov veľká časť výdavkov reaguje na rast nominálnej ekonomiky s oneskorením. Vývoj verejných financií je zároveň negatívne ovplyvnený aj legislatívnymi opatreniami prijatými v predchádzajúcom období, ktoré navyšujú výdavky verejnej správy na celom horizonte rozpočtu[5].

- V roku 2024 môže podľa odhadu Rady dosiahnuť deficit 6,1 % HDP, čo je vyššie len o 0,1 % HDP ako uvádza rozpočet, pričom v rámci štruktúry rozpočtu boli identifikované tak negatívne ako aj pozitívne riziká. Na rozdiel od vládou predpokladaného medziročného poklesu deficitu o 0,5 % HDP očakáva však RRZ, po správnom vykázaní energo pomoci, naopak nárast deficitu a to o 0,4 % HDP. Z tohto pohľadu nie je možné hodnotiť zámer znížiť medziročne deficit o 0,5 % HDP ako realistický bez dodatočných opatrení. Ak by mal rozpočet spĺňať výdavkové limity, deficit by mal poklesnúť z očakávaných 5,7 % HDP v roku 2023 na 5,2 % HDP v tomto roku pomocou trvalých opatrení.

- Rezerva na kompenzačné opatrenia súvisiace s rastom cien energií je rozpočtovaná vo výške 800 mil. eur, čo nepostačuje na financovanie schválených kompenzačných schém v roku 2024, kde očakávané náklady predstavujú 1,25 mld. eur. Rozpočet predpokladal financovanie dodatočných výdavkov z prostriedkov EÚ z refundácie programu SAFE, tento pozitívny vplyv sa však podľa metodiky ESA 2010 v plnej miere s najväčšou pravdepodobnosťou zaznamená do výsledkov hospodárenia roku 2023[6]. Po zohľadnení tohto vplyvu RRZ odhaduje v roku 2024 vyššiu úroveň jednorazových opatrení v deficite o 0,3 % HDP.

- V porovnaní s rozpočtom pre rok 2024 RRZ prognózuje nižšiu úroveň deficitu bez jednorazových opatrení o 0,1 % HDP. Táto pozitívna odchýlka vyplýva predovšetkým z nižšieho očakávaného čerpania výdavkov štátneho rozpočtu, kde RRZ nepredpokladá vyčerpanie celého objemu rozpočtových rezerv a identifikovala úsporu vo výdavkoch v rezorte obrany. Nižšie čerpanie očakáva RRZ aj v sociálnych dávkach, predovšetkým vo výdavkoch na rodičovský príspevok. Na druhej strane, negatívne riziká pre schodok rozpočtu RRZ identifikovala vo výnose daňových príjmov a vo výdavkoch na zdravotníctvo.

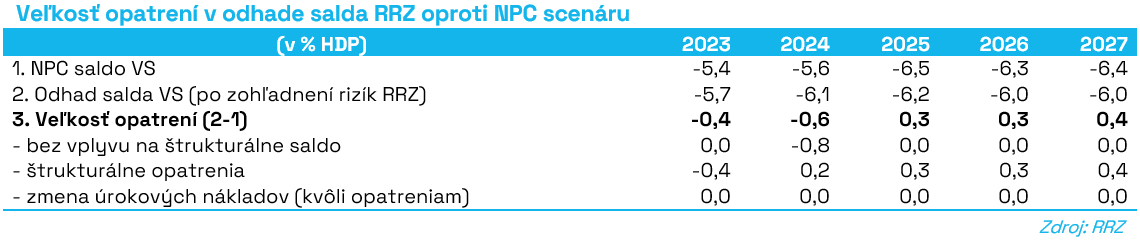

- V nasledujúcich rokoch Rada odhaduje pokles deficitu na 6,2 % HDP v roku 2025 a 6,0 % HDP v rokoch 2026 a 2027. V roku 2026 je odhad o 0,4 % vyšší ako schodok rozpočtu podľa MF SR, a preto rozpočet zostavený v tomto roku nie je možné považovať za realistický. Navyše, voči deklarovaným cieľom chýbajú vláde vyšpecifikované opatrenia v hodnote 1,2 % HDP v roku 2025 a 2,0 % HDP v 2026.

- Trvalé opatrenia podľa odhadu RRZ prispievajú v rokoch 2023 až 2027 k zhoršeniu deficitu kumulatívne o 0,3 % HDP, a to hlavne kvôli opatreniam trvale zvyšujúcim výdavky. Ide najmä o zavedenie 13. dôchodkov, zvýšenie výdavkov na zdravotnú starostlivosť, zvýšenie výdavkov súvisiacich so zriadením nového ministerstva, ako aj predpokladané čerpanie časti legislatívnej rezervy určenej na nové vládne politiky. Tie by mali byť čiastočne kompenzované opatreniami na strane príjmov (zvýšením sadzieb spotrebných daní, zavedením daňových licencií, trvalou časťou znovuzavedeného bankového odvodu), ako aj predpokladom RRZ o znížení investícií samospráv v dôsledku ich aktuálnej nepriaznivej finančnej situácie (s vplyvom 0,2 % HDP). Preto samotná vláda prispieva rozpočtom k trvalému zhoršeniu o 0,5 % HDP.

- Na základe svojej strednodobej fiškálnej prognózy Rada vypočítala sumu výdavkov, ktoré spadajú pod limit verejných výdavkov a pozrela sa tak, ako by v jej odhade vyzeralo plnenie tohto limitu zo strany vlády. Potreba konsolidačných opatrení – ak by vývoj verejných financií bol v súlade s RRZ scenárom – pre splnenie limitu verejných výdavkov dosahuje sumu 1,2 mld. eur v roku 2024 a postupne rastie až na úroveň 3,1 mld. eur v roku 2027. V porovnaní s výškou konsolidačných opatrení, ktorá vyplýva z rozpočtu, je suma konsolidačných opatrení v odhade RRZ nižšia o takmer 500 mil. eur v roku 2024 a naopak vyššia o takmer 850 mil. eur v roku 2026. V roku 2025 sa odhad RRZ a MF SR zásadne neodlišuje. Rozdiel v odhade roku 2024 je tvorený predovšetkým nižším odhadom výdavkov na obranu, predpokladaným nečerpaním časti zdrojov v rozpočtovej rezerve a nižšou prognózou výdavkov na rodičovský príspevok. V ďalších rokoch sa situácia otočí z dôvodu chýbajúcej indexácie výdavkov zo strany MF SR.

- Splnenie limitu verejných výdavkov v rokoch 2024 až 2027 by viedlo k zníženiu deficitu na 3,7% HDP do roku 2027 a k nižšiemu hrubému dlhu oproti súčasnému odhadu RRZ o 6,4b. na úrovni 62,2 % HDP na konci roku 2027. Táto úroveň deficitu by nepostačovala na stabilizovanie podielu dlhu na HDP.

- Na základe odhadu vývoja salda verejnej správy RRZ očakáva, že podiel hrubého dlhu na HDP za rok 2023 klesol na 56,8 % HDP. Po medziročnom poklese hrubého dlhu v pomere k HDP v rokoch 2022 a 2023, najmä vplyvom vysokej inflácie, vzrastie v strednodobom horizonte hrubý dlh verejnej správy podľa RRZ až na úroveň 68,6 % HDP na konci roku 2027. Vzhľadom na postupný pokles hraníc sankčných pásiem by to znamenalo, že dlh bude zotrvávať vysoko nad horným limitom dlhovej brzdy, pričom v roku 2027 ho bude prevyšovať až o takmer 19 p.b.

- Čistý dlh by dosiahol na konci roku 2023 úroveň 49,5 % HDP. Úroveň čistého dlhu by sa pri predpokladoch RRZ o postupnom poklese hotovostnej rezervy štátu počas strednodobého horizontu na historický priemer v predkrízovom období, mala zvýšiť na 62,7 % HDP na konci roku 2027, čo by znamenalo historicky najvyššiu úroveň.

- Schválený rozpočet verejnej správy prispieva podľa odhadu RRZ k zhoršeniu ukazovateľa dlhodobej udržateľnosti o 0,2 % HDP. Negatívny príspevok opatrení vlády je ešte vyšší a dosahuje 0,5 % HDP. Súvisí to aj s tým, že významná časť schválených opatrení zlepšuje saldo v strednodobom horizonte len dočasne s následným zhoršovaním stavu verejných financií v dlhodobom horizonte. K odhadovanému zmierneniu ukazovateľa dlhodobej udržateľnosti celej verejnej správy o 0,2 % HDP oproti príspevku vlády vedie predpoklad RRZ o znížení investícií samospráv v dôsledku ich aktuálnej nepriaznivej finančnej situácie. Nakoľko výdavkové limity vyžadujú od vlády naopak zlepšovanie udržateľnosti o 0,5 % HDP ročne, neplnenie výdavkových rozpočtov znamená zhoršovanie udržateľnosti vládou až o 1 % HDP (0,5 % + 0,5 %), čo korešponduje s vyššie uvedenou potrebou dodatočných opatrení vo výške 1,2 mld. eur.

- RRZ odhaduje, že fiškálna expanzia dosiahla v roku 2023 úroveň 5,3 % HDP, k čomu prispelo najmä výrazné zrýchlenie čerpania EÚ fondov z dôvodu končiaceho sa tretieho programového obdobia. Odhadovaný výrazný prepad v čerpaní EÚ fondov v strednodobom horizonte sa podľa RRZ premietne do reštriktívneho nastavenia fiškálnej politiky, napriek nárastu štrukturálneho deficitu, ktorý prispieva k fiškálnej expanzii. Nakoľko v strednodobom horizonte bude ekonomika operovať mierne nad svojim potenciálom, výraznejšia konsolidácia nad rámec vývoja aktuálne odhadovaného RRZ by nemala zásadným vplyvom spôsobovať nerovnováhy v ekonomike, naopak bola by želateľná s ohľadom na aktuálny stav a vývoj verejných financií. Z pohľadu makroekonomických efektov fiškálnej politiky je preto žiadúce, aby nevyhnutná konsolidácia verejných financií bola sprevádzaná čo najintenzívnejším čerpaním EÚ fondov.

- Rada považuje plnenie výdavkových limitov za minimálne tempo ozdravovania verejných financií a toto by mali rešpektovať aj rozpočtové ciele. V takom prípade by rozpočtové ciele deficitu dosiahli výšku 5,2 % HDP v roku 2024, 4,5 % HDP v roku 2025 a 3,9 % HDP v roku 2026. Aktuálne rozpočtové ciele sú tak vyššie o 0,8 % HDP v roku 2024, o 0,5 % HDP v roku 2025 a o 0,1 % HDP v roku 2026. Samotné rozpočtované zhoršenie stavu verejných financií v roku 2024 a odsúvanie potrebnej konsolidácie do ďalšieho obdobia nepovažuje Rada vzhľadom na nepriaznivý stav verejných financií a končiace sa krízové obdobie za opodstatnené. V strednodobom horizonte do roku 2026 by teda mala byť podľa RRZ hlavným cieľom vlády stabilizácia dlhu prostredníctvom zníženia deficitu blízko hranice 3 % HDP a zníženie vysokého rizika dlhodobej udržateľnosti bezpečne do pásma stredného rizika.

- Zároveň, napriek nárastu daňovo-odvodového zaťaženia sa nedosiahlo zlepšenie stavu verejných financií. To prirodzene zužuje priestor pre potrebnú konsolidáciu na strane príjmov do budúcnosti. Rada by chcela apelovať, aby v súlade so snahou podporiť dlhodobú konkurencieschopnosť Slovenskej republiky s prihliadnutím na požiadavku ekonomickej a sociálnej spravodlivosti a solidarity medzi súčasnými a budúcimi generáciami, boli všetky príjmové a výdavkové opatrenia v súlade s princípmi transparentnosti a efektívnosti dôsledne zvažované a v riadnom legislatívnom procese dostatočne odôvodňované.

- Z pohľadu transparentnosti rozpočet podľa RRZ nie je zostavený v súlade s rozpočtovými cieľmi na roky 2024 až 2026. V roku 2024 je cieľ rozpočtu podľa vlády naplnený aj zaznamenaním financovania časti energopomoci zo zdrojov EÚ, čo je s veľkou pravdepodobnosťou v rozpore s princípmi ESA2010. Vďalších rokoch chýbajú konkrétne konsolidačné opatrenia.

[1] RRZ, Predbežný výpočet aktualizácie limitu verejných výdavkov, december 2023. Na účely hodnotenia rozpočtu RRZ uvažuje s tými výdavkovými limitmi, ktoré by platili po splnení všetkých zákonných postupov (schválenie vypočítaných limitov v NR SR zo dňa 15. decembra 2023 a ich aktualizácia na súčasný stav legislatívy).

[2] V porovnaní s limitmi, ktoré NR SR schválila vo februári 2023 a ktoré sú podľa názoru RRZ stále platné, prekračuje rozpočet verejnej správy limit o 5 miliárd eur v roku 2024 a o 5,9 miliardy v roku 2025. Hlavným dôvodom týchto výrazných odchýlok je to, že tieto boli limity vypočítané koncom roku 2022 (na základe vtedajšieho stavu legislatívy) a vyžadujú tak kompenzáciu negatívnych vplyvov opatrení prijatých v priebehu roku 2023.

[3] Viď kapitola 7.

[4] Viď kapitola 7.

[5] Pre podrobnejší výpočet jednotlivých faktorov viď tu.

[6] Stanovisko Európskej komisie k Návrhu rozpočtového plánu na rok 2024 Slovenskej republiky, str. 4.